Restatements began to accelerate in 2001 — before the accounting scandals that launched SOX — particularly for companies trading off the major exchanges.

Thomson Tax & Accounting reports a Treasury Department study that reviewed 10 years of data found that the dramatic increase in financial restatements began long before the passage of the Sarbanes-Oxley Act of 2002.

“The uptick in the amount of restatements started before Sarbanes-Oxley in 2002, and yet a lot of people said [it] was the cause of the increases,†said David Nason, the Treasury Department’s Assistant Secretary for Financial Institutions, in an April 9, 2008, briefing in Washington, DC.

The key driver seems to be the economy. If history repeats, then we could be seeing another surge with this downturn.

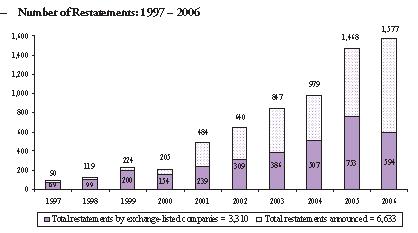

A mere 90 were filed in 1997. That number climbed to 640 in the year Sarbanes-Oxley was enacted, according to the study, titled “The Changing Nature and Consequences of Public Company Financial Restatements” [Get the free download: 57 pages, PDF]. Much of the increase from 2000 to 2002 was attributed to the dot-com bubble and its aftermath. By 2006, the most recent year tracked in the study, the number of restatements hit 1,577.

A mere 90 were filed in 1997. That number climbed to 640 in the year Sarbanes-Oxley was enacted, according to the study, titled “The Changing Nature and Consequences of Public Company Financial Restatements” [Get the free download: 57 pages, PDF]. Much of the increase from 2000 to 2002 was attributed to the dot-com bubble and its aftermath. By 2006, the most recent year tracked in the study, the number of restatements hit 1,577.

The study, which draws no policy conclusions or recommendations, was commissioned by Treasury Secretary Henry Paulson (pictured) in May 2007 as part of his capital markets competitiveness initiative. The study will have implications for the Securities and Exchange Commission (SEC), which is examining proposals on financial restatements from its Advisory Committee on Improvements to Financial Reporting (CIFR). CIFR’s draft report, released in February for public comment, included a proposal that some investors fear will relax the rules on reporting accounting errors.

Key excerpt:

The U.S. Treasury Department commissioned this study to investigate the increase in public company restatement activity over the decade from 1997 to 2006. Th e purpose is to understand characteristics and consequences of financial statement restatements for violations of U.S. Generally Accepted Accounting Principles (GAAP) over this decade. The study analyzes 6,633 restatements of financial results announced over this period. Th ese are the broad findings:

• It is well-known that restatements increased in recent years; over the decade, they grew nearly eighteen-fold, from 90 in 1997 to 1,577 in 2006. However, the increase is largely driven by companies that do not trade on the major stock exchanges. Non-exchange-listed companies account for only 23% of all restatements in 1997, but increase to 62% by 2006.

• Restatement frequencies begin to accelerate in 2001-well in advance of the passage of the Sarbanes-Oxley Act of 2002 (SOX). This acceleration is likely due in part to the economic downturn about this time.

• The average market reaction to restatement announcements is negative throughout the study period. However, beginning in 2001, the magnitude of market reactions declines notably. This decline coincides with an increase in the number of restatements between 2001 and 2006.

• In particular years, restatement frequencies and market reactions are associated with several disparate factors. These include overall market returns and volatility, regulatory activities, and changes in the mix of underlying accounting issues. Regarding the shift in accounting issues:

—- Restatements attributed to fraud and those aff ecting revenues tend to have more negative market reactions. However, the percentages of both fraud and revenue restatements decline over the decade. Fraud is a factor in 29% of all 1997 restatements, but only 2% of 2006 restatements.2 Th e proportion of revenue restatements also decreases, from 41% in 1997 to 11% in 2006.

—- On the other hand, restatements related to accounting for non-operating expenses, non-recurring events and reclassifications typically do not have discernibly negative market reactions. Together, these groups represent about 24% of all 1997 restatements, increasing to nearly half at the end of the study period.

• Across the decade, the average restating company increases in size, but remains similar to a comparison group of non-restating companies. Companies of differing sizes tend to restate different accounting issues, and several of the distinctions are consistent with expected variations in the activities of larger versus smaller

companies.

• Finally, restating companies are typically unprofitable even before the restatement. In the year prior to announcing a restatement, more than half of restating companies report a net loss.

For another view:

See http://www.cpasuccess.com/2008/04/rethinking-rest.html, which states: the report is an “eye-opening example of Sarbanes-Oxley’s impact on corporate finance.”