Cornerstone Report

By CPA Trendlines Research

The Internal Revenue Service has a long and complex history dating back to the early days of the United States. The story of the IRS intersects at critical points with the development of the tax, accounting and CPA profession.

The current federal income tax can be traced back to the Revenue Act 1913, passed after the states ratified the 16th Amendment to the Constitution. The act provided that taxes on individual taxpayers would be imposed beginning in 1913 on incomes of $3,000 and up.

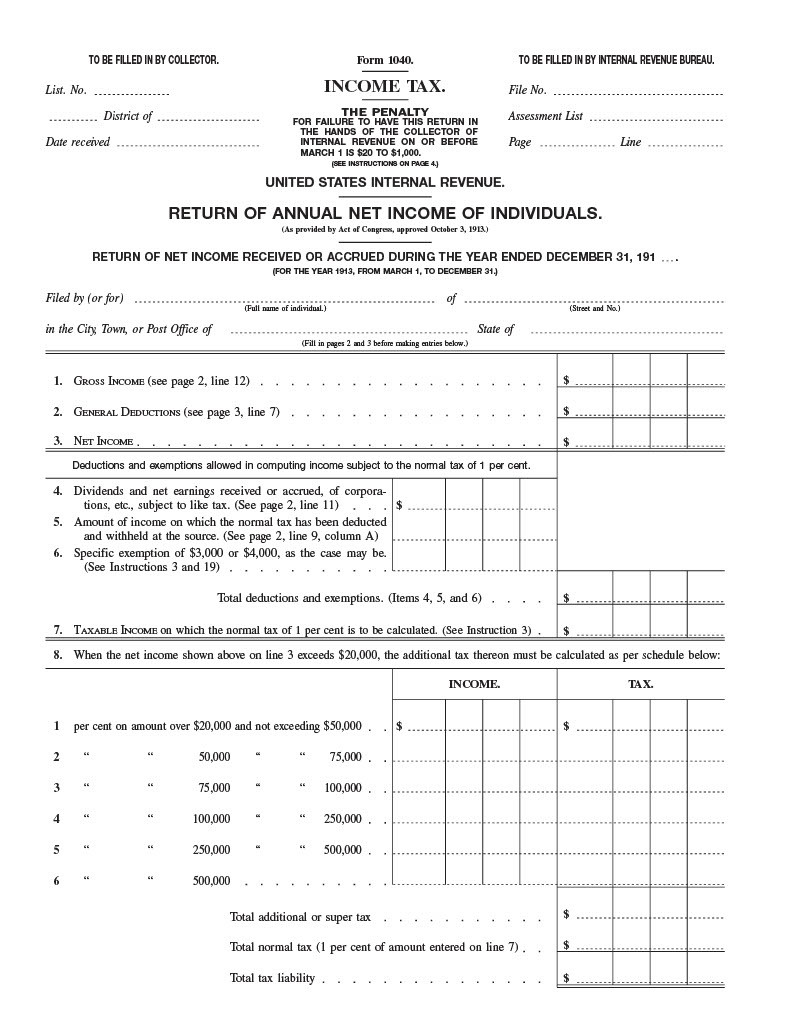

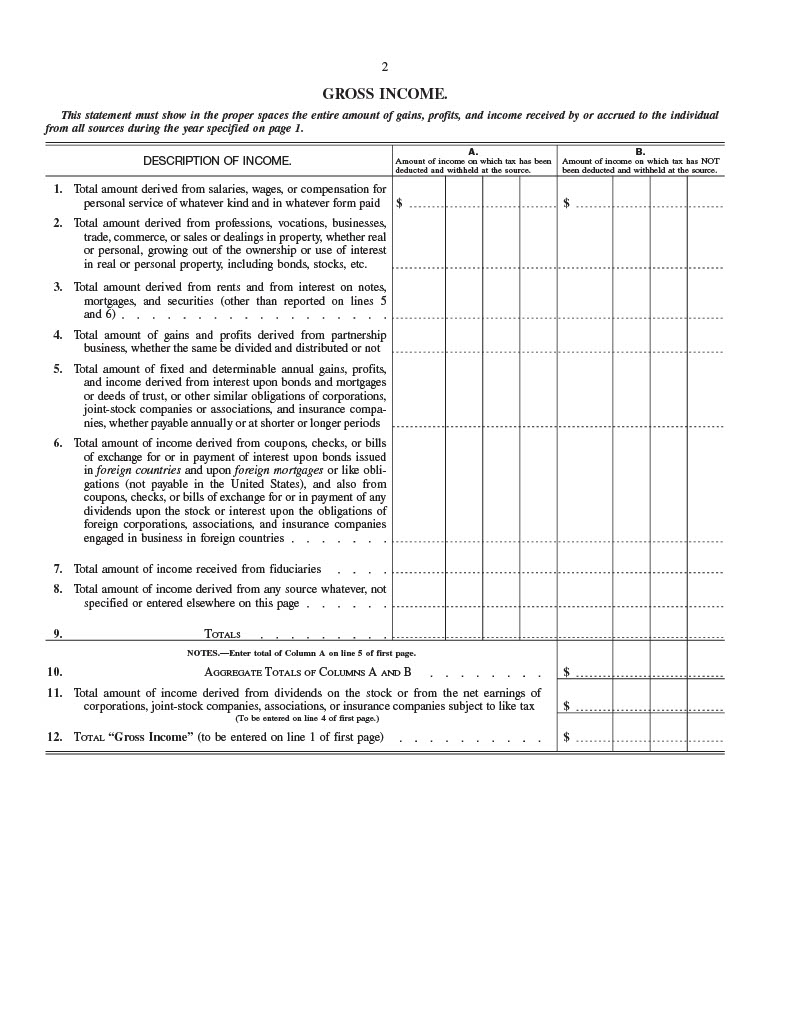

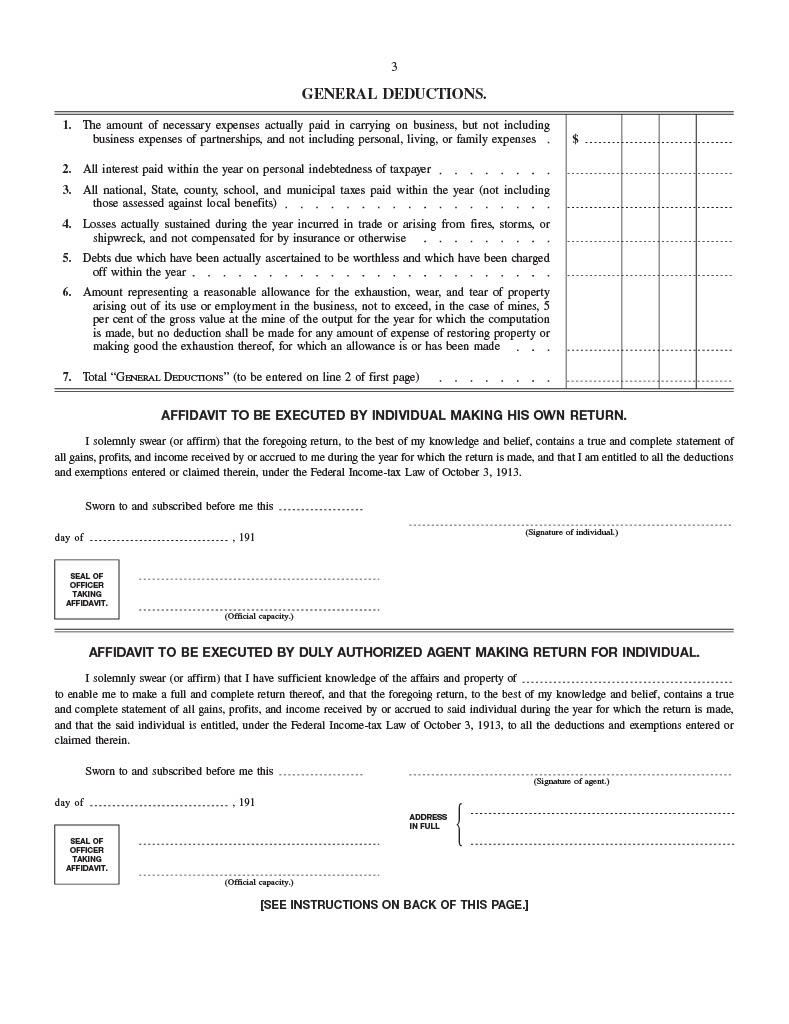

The modern Form 1040 can be traced back to the original form, with photos to the right and below. This form is reproduced from Federal legislation, 1913-1914: income tax, war revenue, federal reserve bank, anti-trust and trade commission laws, published by the Federal Legislative Bulletin Service in 1915.

The Law Library of Congress has an extensive collection of materials concerning the history of federal taxation, including bills, committee reports, and laws. Many of these sources can be accessed through Congress.gov or in specific databases available onsite at the Library of Congress.

The O.G. Tax Form: Form 1040, 1913

Just three pages and one page of instructions.

Download the first IRS tax form, the 1913 Form 1040, here (PDF)

The roots of federal taxation in the United States can be traced back to 1791 when Congress approved a law establishing a tariff system on imports and an internal excise tax on whiskey. This led to the creation of the Office of the Commissioner of Revenue by Treasury Secretary Alexander Hamilton, which is considered the predecessor to today’s IRS.

The modern IRS has its origins in the American Civil War. In 1862, President Abraham Lincoln and Congress passed the Revenue Act, which created the office of Commissioner of Internal Revenue and instituted the first federal income tax to help fund the Union’s war efforts. This tax was initially set at 3 percent on incomes over $800, exempting most wage earners.

The income tax was repealed in 1872 after the Civil War. However, the debate over federal income taxation continued as the country grew and federal responsibilities expanded. In 1894, a new income tax was briefly instituted but was quickly declared unconstitutional by the Supreme Court.

The pivotal moment in IRS history came with ratifying the 16th Amendment to the U.S. Constitution in 1913. This Amendment granted Congress the authority to levy a federal income tax without apportioning it among the states. Following this, the Revenue Act of 1913 was passed, officially establishing the federal income tax and creating the Bureau of Internal Revenue.

Over the following decades, the IRS’s responsibilities grew significantly:

1. In 1918, income tax rates were raised to 77 percent to fund World War I.

2. The Social Security Tax was introduced in 1935.

3. The Unemployment Insurance Tax was implemented in 1939.

4. During World War II, withholding taxes from employee wages was introduced.

In 1953, the Bureau of Internal Revenue was officially renamed the Internal Revenue Service. Since then, the IRS has undergone numerous reforms and reorganizations, particularly in the 1990s. It has also embraced technological advancements, transitioning from manual processing to computerized systems in the late 1950s.

Today, the IRS collects nearly $5 trillion in tax revenue annually.

Timeline

The modern IRS has its roots in the Civil War era:

– In 1862, President Lincoln and Congress created the Office of Commissioner of Internal Revenue to help fund the Civil War effort.

– This office later became known as the Bureau of Internal Revenue.

– In 1953, the agency was officially renamed the Internal Revenue Service to focus more on serving the public rather than merely collecting taxes.

Several significant tax reforms affected the IRS in the 20th century:

– World War I (1918): Income tax rates were raised to 77 percent to fund the war effort.

The New Deal (1930s) introduced new taxes, including the Social Security Tax in 1935.

– World War II: Tax rates increased dramatically, reaching 94 percent for top earners by 1944.

– 1980s: The Reagan administration implemented major tax cuts and reforms, including lowering the top tax rate from 50 percent to 28 percent.

– 1998: The IRS Restructuring and Reform Act led to a comprehensive review and restructuring of the agency.

The Revenue Act of 1862 was crucial for funding the Union’s war effort:

– It established the first federal income tax in the United States.

– The act imposed a 3 percent tax on incomes between $600 and $10,000 and a 5 percent tax on incomes over $10,000.

– By the end of the Civil War, this income tax had raised $347 million, a substantial sum.

The 16th Amendment, ratified in 1913, played a pivotal role in establishing the modern IRS:

– It granted Congress the authority to levy a federal income tax without apportioning it among the states.

– This Amendment overcame earlier Supreme Court rulings that had declared income taxes unconstitutional.

– Following its ratification, Congress passed the Revenue Act 1913, officially establishing the federal income tax and creating a permanent Bureau of Internal Revenue.

The implementation of the first federal income tax was not without challenges:

– No taxes were collected in the first year after the 16th Amendment’s ratification. The IRS (then the Bureau of Internal Revenue) checked tax forms for accuracy.

– The agency’s workload increased tenfold, triggering a massive restructuring.

– Professional tax collectors began to replace a system of “patronage” appointments.

– The IRS doubled its staff but was still processing 1917 returns in 1919, indicating the magnitude of the challenge.

This transition period was marked by significant growing pains as the agency adapted to its new responsibilities and the American public adjusted to the concept of a federal income tax.

- The first U.S. federal income tax was introduced in 1861 to help fund the Civil War.

- This period saw an increased need for financial record-keeping, boosting the importance of accounting practices.

1887: Formalization of the Accounting Profession

- The American Association of Public Accountants (AAPA) was established, marking the formal recognition of accounting as a profession in the U.S.

- This coincided with growing discussions about implementing a permanent federal income tax.

1913: 16th Amendment and Modern Income Tax

- The 16th Amendment was ratified, allowing Congress to levy an income tax without apportioning it among the states.

- The Revenue Act of 1913 established the modern federal income tax system.

- This created a significant demand for accountants skilled in tax preparation and planning.

1917-1918: World War I and Tax Complexity

- Income tax rates were raised dramatically to fund the war effort, reaching up to 77 percent for top earners.

- The increased complexity of tax laws led to a growing need for specialized tax accountants.

1934: Securities Exchange Act

- This act required public companies to file periodic financial reports certified by independent public accountants.

- It significantly increased the role of accountants in ensuring corporate compliance with financial reporting and tax regulations.

1939: Internal Revenue Code

- The first consolidated set of tax laws was published as the Internal Revenue Code 1939.

- This codification of tax laws further solidified the need for specialized tax accounting expertise.

1950s-1960s: Rise of Computerization

- Both the IRS and accounting firms began adopting computer technology for data processing.

- This technological shift transformed accounting practices and tax administration.

1986: Tax Reform Act

- This major overhaul of the tax code simplified some aspects of taxation but also introduced new complexities.

- It led to significant changes in accounting practices related to tax planning and compliance.

2002: Sarbanes-Oxley Act

- While primarily focused on corporate governance, this act had significant implications for accounting practices and tax reporting.

- It increased the importance of internal controls in financial reporting, including tax-related matters.

2017: Tax Cuts and Jobs Act

- This major tax reform bill significantly altered the tax code, affecting individual and corporate taxation.

- It required accountants to adapt their practices to the new tax landscape quickly.

The development of technology has significantly impacted the accounting profession over the years. Here are some key milestones in technological advances that have shaped modern accounting:

Early Mechanical Aids

– 1880s – 1890s: Adding Machines and Calculators

– The introduction of mechanical adding machines and calculators greatly improved the speed and accuracy of basic accounting calculations.

Computer Age Begins

– 1950s – 1960s: Mainframe Computers

– Large corporations began using mainframe computers for accounting tasks, marking the beginning of computerized accounting.

– 1970s: Personal Computers

– The advent of personal computers made computerized accounting accessible to smaller businesses and individual accountants.

Software Revolution

– 1983: Introduction of QuickBooks

– The release of QuickBooks marked a significant milestone in user-friendly accounting software for small businesses.

– 1990s: Enterprise Resource Planning (ERP) Systems

– ERP systems integrate various business processes, including accounting, into a comprehensive software solution.

Internet Era

– Late 1990s – Early 2000s: Internet – Based Accounting Software

– The rise of internet-enabled cloud-based accounting solutions allows remote access and real-time collaboration.

Advanced Technologies

– 2010s: Big Data and Analytics

– The ability to process and analyze large volumes of financial data provided new insights and predictive capabilities.

– 2010s – Present: Artificial Intelligence and Machine Learning

– A.I. and ML technologies began automating complex accounting tasks and improving fraud detection.

– 2010s – Present: Blockchain Technology

– Blockchain started to be explored for its potential to enhance the security and transparency of financial transactions.

Mobile and Cloud Computing

– 2010s – Present: Mobile Accounting Apps

The proliferation of smartphones led to the development of mobile accounting applications, which enable on-the-go financial management.

– 2010s – Present: Cloud – Based Accounting Platforms

– Cloud computing revolutionized data storage and access, allowing real-time financial reporting and collaboration.

Automation and Integration

– 2015 – Present: Robotic Process Automation (RPA)

– RPA tools began automating repetitive accounting tasks, significantly improving efficiency.

– 2010s – Present: API Integrations

– Developing APIs allowed for seamless integration between different financial and business software systems.

Emerging Technologies

– 2020s: Advanced Data Analytics and Predictive Modeling

– Sophisticated analytics tools enable more accurate forecasting and decision-making.

– 2020s: Natural Language Processing

– NLP is being used to automate the interpretation of financial documents and generate reports.

These technological advancements have transformed the accounting profession from a largely manual, paper-based practice to a highly automated, data-driven field. They have not only improved efficiency and accuracy but also expanded the role of accountants from mere number crunchers to strategic business advisors.

Cloud computing, artificial intelligence, blockchain, machine learning, and real-time data accessibility have all significantly transformed the accounting profession in recent years. Here’s an overview of how each technology has impacted accounting:

Cloud Computing in Accounting

Cloud computing has revolutionized the accounting profession in several key ways:

– Accessibility and Collaboration: Cloud-based accounting software allows accountants and clients to access financial data anytime, facilitating real-time collaboration.

Cost Efficiency: Cloud solutions reduce I.T. costs by eliminating the need for expensive on-premise hardware and software.

Scalability: Cloud-based systems can easily scale up or down based on business needs without significant infrastructure changes.

– Automatic Updates: Cloud software is automatically updated, ensuring accountants can always access the latest features and compliance requirements.

– Enhanced Data Security: Cloud providers often offer advanced security measures, including encryption and regular backups.

Benefits of A.I. in Accounting

Artificial Intelligence has brought numerous benefits to the accounting field:

– Automation of Repetitive Tasks: A.I. can automate routine accounting tasks like data entry, invoice processing, and bank reconciliations, freeing up accountants for more strategic work.

– Improved Accuracy: A.I.-powered systems can process large volumes of data with minimal errors, reducing the risk of human mistakes.

– Advanced Analytics: A.I. enables sophisticated data analysis, identifying patterns and trends that humans may not detect easily.

– Fraud Detection: A.I. algorithms can detect anomalies and potential fraudulent activities more efficiently than traditional methods.

– Enhanced Forecasting: A.I. can analyze historical financial data and external factors to generate more accurate forecasts.

Blockchain’s Influence on Accounting

Blockchain technology is beginning to impact accounting practices in several ways:

– Enhanced Security and Transparency: Blockchain’s immutable ledger provides a secure and transparent record of all transactions.

– Real-Time Reporting: Blockchain enables real-time recording and reporting of financial transactions.

– Triple-Entry Accounting: Blockchain supports the concept of triple-entry accounting, where a third, immutable entry is created for each transaction.

Smart Contracts: Blockchain-based smart contracts can automate various accounting processes, reducing the need for intermediaries.

Machine Learning in Modern Accounting

Machine learning, a subset of A.I., plays a crucial role in modern accounting:

– Pattern Recognition: ML algorithms can identify patterns in financial data, helping to predict future trends or detect anomalies.

– Automated Categorization: ML can automatically categorize transactions, streamlining the bookkeeping process.

– Risk Assessment: Machine learning models can assess financial risks more accurately by analyzing vast amounts of data.

– Personalized Insights: ML can provide tailored financial insights and recommendations based on a company’s specific financial patterns and industry trends.

Real-Time Data Accessibility

Real-time data accessibility has transformed the way accountants work:

Immediate Decision Making: Accountants can now provide immediate insights and recommendations based on up-to-the-minute financial data.

Proactive Financial Management: Real-time data allows for proactively identifying and addressing financial issues before they escalate.

– Enhanced Client Relationships: Accountants can offer clients more timely and valuable advice, strengthening their advisory role.

Improved Cash Flow Management: Real-time visibility into cash flow enables more effective financial planning and management.

Streamlined Auditing: Real-time access to financial data can make auditing processes more efficient and less time-consuming.