After hundreds of deals, the data show a gravitational pull toward a handful of buyers now driving the profession’s future.

CPA Trendlines PE Deal Tracker: Mega-aggregators are dominating the money flow as the race tightens between Ascend, Ryan LLC, Crete Professionals Alliance, Aprio, Sorren, and Doeren Mayhew.

By CPA Trendlines Research

The frantic pace of deal-making in March has officially transitioned the accounting industry from a “consolidation phase” into a “platform war.”

As the first quarter concludes, the narrative is no longer just about who is buying whom, but about which investment philosophy—and which technology stack—will dominate the next decade.

The conventional narrative about private equity in accounting says capital is flooding in, the profession is democratizing, and every CPA firm in America can access institutional money for the first time. But the cold, hard data tells a different story.

MORE in Private Equity | Alan Whitman Plants a Flag in the Private Equity Landscape | The PE Takeover: Audit Problem? What Audit Problem? | The 7.6x Machine: How Grassroots Firms Are Taking Private Equity for a Ride | Why the Next Big CPA Firms Won’t Look Like CPA Firms

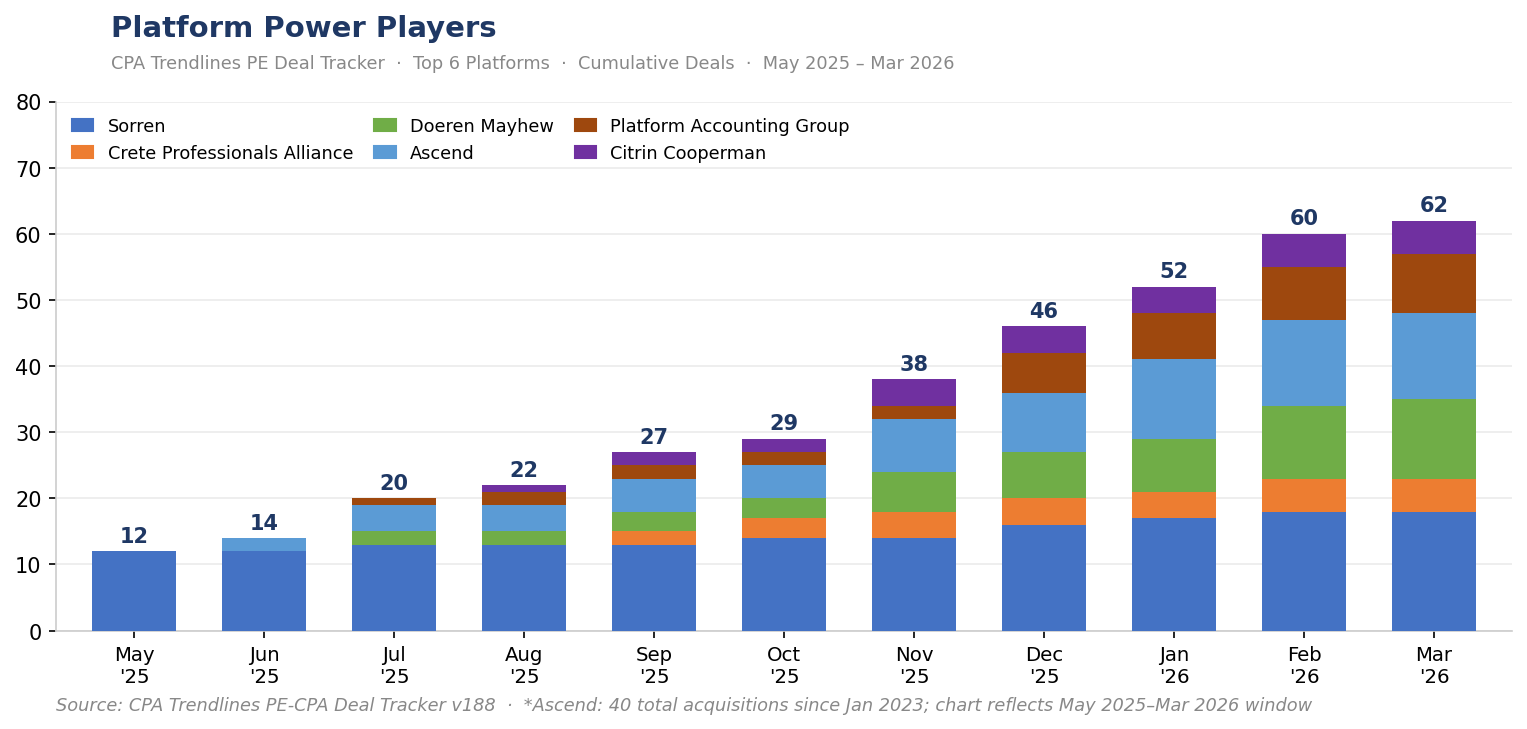

Of the 400-odd transactions logged in the CPA Trendlines PE-CPA Deal Tracker™ since 2016, about 155, or 39 percent, of deals are concentrated in just six platforms: Ascend, Ryan LLC, Crete Professionals Alliance, Aprio, Sorren, and Doeren Mayhew That challenges the notion of a market open to all.

The idea that PE would spread evenly across hundreds of firms, like a broad revolution, is, in the actual deal flow, a rapid gravitational implosion around a handful of mega-aggregators that are vacuuming up firms faster than the rest of the market combined. The acceleration curve alone should unsettle anyone clinging to the idea that this market is still nascent.

The tracker recorded a handful of deals in all of 2021, the year TowerBrook Capital Partners took its majority stake in EisnerAmper in July 2020 and shattered the profession’s private-equity virginity.

By 2022, the count climbed to 19. In 2023, it hit 48. In 2024, 79. Then came 2025, with 170 transactions, a record that more than doubled the prior year and marked the moment PE capital stopped knocking politely on accounting’s door and kicked it open.

Through March 2026, the tracker shows 67 deals in the first quarter alone, a pace that, if sustained, would approach 340 by year’s end.

“The rate of change in the last five years has been insane,” says Allan Koltin, the CEO of Koltin Consulting Group, who has advised on more of these transactions than anyone in the profession.

But velocity alone does not capture the market’s true shape. All six of those dominant platforms — Ascend, Ryan, Crete, Aprio, Sorren, and Doeren Mayhew — were active buyers in the first quarter of 2026. They are not pausing, and the firms orbiting outside their gravitational pull are running out of room.

“The dirty, dark secret is there are way more buyers than eligible firms,” says Koltin, who has personally advised EisnerAmper on a majority of its post-TowerBrook deals.

That paradox — a market drowning in capital but starving for qualified sellers — is the engine driving concentration. When eligible targets are scarce, the platforms with the earliest head starts, the largest war chests, and the most developed integration playbooks win disproportionately.

The top 10 platforms account for more than half of all deal activity.

Top 10 Platforms, by Number of Deals

| Rank | Platform Firm | PE Sponsors | Total Deals |

| 1 | Ascend | Alpine Investors | 40* |

| 2 | Ryan LLC | Ares Management; Neuberger Berman; Onex | 27 |

| 3 | Crete Professionals Alliance | Thrive Capital; Bessemer Venture Partners | 25 |

| 4 | EisnerAmper | TowerBrook Capital Partners | 23 |

| 4 | Aprio | Charlesbank Capital Partners | 24 |

| 6 | Sorren | DFW Capital Partners | 21 |

| 7 | Doeren Mayhew | Audax Private Equity | 18 |

| 8 | Platform Accounting Group | The Cynosure Group | 15 |

| 9 | Dains LLP | PAI Partners | 13 |

| 10 | Citrin Cooperman | New Mountain Capital; Blackstone | 10 |

* 40 total acquisitions as of December 31, 2025, per Alpine Investors 2025 Year-in-Review; includes 18 deals completed in 2025. Source: alpineinvestors.com/update/2025-year-in-review/

Ascend in 1st Place

Ascend leads the tracker with 40 total acquisitions since launching in January 2023 — including 18 new deals in 2025 — making it the most active acquirer in the PE-backed accounting profession by total deal count.

David Wurtzbacher founded Ascend with Alpine Investors as its backer, pitching a model he described as an alternative to the traditional partnership structure rather than a straightforward roll-up. The distinction matters to him.

It reached Accounting Today Top 100 status within six months and now sits at No. 24 on Accounting Today’s 2026 Top 100 with $590 million in net revenue and more than 2,600 employees across 22-plus partner firms in 13-plus states.

What distinguishes Ascend from the aggregators above it in revenue but below it in deal count is its insistence on preserving the operating identity of each partner firm. Acquired firms — from Opsahl Dawson in Vancouver, Washington, to KSDT in Miami — retain their local leadership, their client relationships, and their brand. The Ascend platform provides capital, technology, recruiting, and back-office infrastructure without imposing a national brand.

Pushing back on skeptics, Wurtzbacher says, “I have found that the profession questions who would want to own a big accounting firm. And that is a pretty uninformed view.”

His comment captures an important asymmetry as accounting insiders debate whether PE belongs in the profession, even as institutional capital has already priced it as a permanent asset class.

Alpine’s 2025 Year-in-Review reported $475 million in pro-forma trailing twelve-month revenue at year-end 2025, with the gap between that figure and Accounting Today’s $590 million reflecting different snapshot dates and methodology. By April 2026, Ascend’s own website cited collective revenue exceeding $700 million, a figure that includes the full platform’s run-rate after 2026 additions.

Ryan LLC

Ryan LLC sits second in the tracker at 27 documented deals, and its trajectory is more vertical than horizontal.G

G. Brint Ryan founded the Dallas tax firm in 1991, surrendered its CPA license in 1998 to operate purely as a tax consultancy, and spent two decades building a global practice that now serves 18,000 clients through 113 locations in 60-plus countries.

Onex Corporation bought 42 percent of Ryan in 2018 at a $1.1 billion valuation. Ares Management invested in 2022, pushing the valuation to $2.5 billion. Then, on Jan. 14, 2026, Neuberger Berman agreed to invest up to $1.2 billion through its Capital Solutions and Private Markets units, valuing Ryan at approximately $7 billion — a 536 percent increase over the Onex entry in eight years, without a single exit event.

David Lyon, head of Neuberger Berman Capital Solutions, calls Ryan “a differentiated platform sitting at the intersection of tax expertise, technology, and client service.” The progression from $1.1 billion to $7 billion with three successive PE sponsors and no flip is itself a data point about the profession’s capacity to compound investor conviction.

Crete

Crete Professionals Alliance, co-founded by Jake Sloane and Frank Zhang in Tampa in 2023 and backed by Thrive Capital, headed by Joshua Kushner, Trump envoy Jared Kushner’s brother, and by Bessemer Venture Partners, exemplifies the aggregator model at full throttle.

Starting with a $500 million war chest, Crete has now absorbed more than 40 partner firms, pushing its annual revenue past $300 million and its workforce to 900 employees across 17 offices, with operations extending into Asia. Its 25 logged transactions place it third in the tracker.

What makes Crete’s model particularly paradoxical is its choice of technology partner: an in-house team collaborating directly with OpenAI engineers to build custom AI tools for accounting — tools that, by one partner firm’s account, save hundreds of hours per month during audit testing.

Crete is, in other words, using tomorrow’s technology to buy yesterday’s firms, most of them built over decades on manual labor and local relationships.

Aprio Adds a Law Firm

Aprio, the Atlanta-based firm with roots dating back to 1952, sits tied for fourth in the tracker with 24 deals. Charlesbank Capital Partners made its first institutional investment in Aprio in July 2024, reportedly after evaluating seven firms in the sector.

Aprio CEO Richard Kopelman has since executed 18 strategic acquisitions since mid-2024, pushing revenue to $615 million and the firm to No. 20 on Accounting Today’s 2026 Top 100 list.

But Aprio’s boldest move may have nothing to do with accounting at all. In early 2026, it combined with Scottsdale-based Radix Law to form Aprio Legal under Arizona’s Alternative Business Structure program, making it one of the first PE-backed accounting platforms to cross into legal services. If the profession’s future is multidisciplinary, Aprio is placing a real-money bet.

Sorren: Not a Garden-Variety Roll-Up

Sorren, at 21 deals, is the youngest platform by calendar age and the most dramatic by birth.

On May 1, 2025, 13 firms — many of them connected through the BDO Alliance — simultaneously combined under a new brand backed by DFW Capital Partners, a New York-based PE firm with more than $2 billion in assets under management.

At launch, Sorren counted 85 partners, $170 million in revenue, and more than 1,000 employees across 20-plus offices. By early 2026 it had added firms in Texas, Oregon, Nevada, and Virginia, climbing to No. 61 on Inside Public Accounting’s Top 100 in its first year of eligibility.

CEO Michael O’Donnell, a Deloitte alumnus, says DFW “has been vital in bringing our vision to life.”

President Josh Tyree is more outspoken. “If all you’re looking to do is do a rollup, that’s probably not our style,” Tyree says.

Whether the market believes that distinction remains to be seen — 13 firms merging overnight under PE capital is difficult to characterize as anything other than a rollup, however aspirational the framing.

Doeren Mayhew: Fast Mover

Doeren Mayhew is the newest entrant to the top tier, and the fastest mover in the tracker by pace. Audax Private Equity backed the Troy, Michigan firm in August 2024, and by mid-March 2026 Doeren had completed 16 disclosed deals — 13 in 2025 alone, and three more in the first quarter of 2026.

That pace — roughly one acquisition per month — is the highest sustained acquisition rate in the tracker for any platform in its first 18 months of PE backing.

The deals span geographies aggressively: Atlanta (twice), Nashville (twice), Houston, Grand Rapids, Rochester, Key Biscayne, Birmingham, and Orlando, among others. The pattern is not regional consolidation. It is national coverage on a compressed timeline.

CEO Mark Gerler has not made the media rounds the way Wurtzbacher or O’Donnell have. Doeren’s approach is quieter than Sorren’s simultaneous 13-firm launch or Ascend’s identity-preservation pitch. But the deal count speaks for itself. At 16 disclosed acquisitions in 18 months, Doeren Mayhew is not coming up fast. It has arrived.

Pssst, Wanna Pay $1.5 Billion for an Accounting Firm?

“If you combined the revenues of the five largest roll-ups into one,” Koltin calculates, “they would be about $1.5 billion and a top 12 accounting firm.”

Gary Shamis, the CEO of Winding River Consulting and a vocal skeptic of PE’s long-term fit in accounting, responds with the question that haunts the model, asking, “What are the exits going to be? Who wants to buy a $1.5 billion CPA firm?”

The concentration thesis is not merely anecdotal. An NBER working paper published in 2025 by Inna Abramova and John M. Barrios, using data from 1999 to 2024 linking more than 3,600 PE transactions to M&A, labor markets, and audit pricing, finds that “PE investment raises labor-market concentration in key accounting occupations and drives up ERISA audit fees.”

After PE entry, the paper concludes, “firms grow faster: non-audit revenues rise, employment expands, and cross-state M&A accelerates, consistent with platform-building and consolidation.” The academic evidence confirms what the deal tracker shows in miniature: capital is not dispersing across the profession. It is pooling.

Lessons from the Insurance Industry

Insurance brokerage, the professional services sector most advanced in its PE consolidation cycle, offers a cautionary mirror.

Since 2008, more than 10,000 M&A transactions have closed in insurance distribution, but the number of unique buyers has dropped from 140 in 2020 to 99 in the first half of 2025, according to OPTIS Partners. The top 10 acquirers now capture roughly 50 percent of all annual deal volume, and PE-backed or hybrid buyers account for more than 72 percent of reported transactions.

Nine of the top 10 insurance acquirers are PE-backed. Accounting follows the same arc, but roughly three to five years behind. The profession’s 50-and-counting PE-CPA platforms may sound like a crowded field, but insurance shows that crowded fields thin relentlessly. Capital concentrates, marginal buyers fall away, and the platforms with the deepest pockets and earliest vintage become self-reinforcing ecosystems.

Eight percent of IPA 500 firms are now PE-backed, representing approximately $11.2 billion of the sector’s roughly $146 billion in total revenue. That may sound modest until you consider that the figure was zero in 2020.

A Sobering Reality

CPA Trendlines Research estimates that private-equity-driven revenue multiples now imply an aggregate enterprise value of more than $400 billion for the Top 500 CPA firm sector, a valuation reset exceeding $200 billion.

But the reality is more sobering. “More than half of the CPA firms in the country won’t qualify to be part of private equity,” Koltin says.

The capital is real. But its accessibility is a myth.

The five-firm simultaneous combination that formed the national Richey May platform on Sept. 9, 2025 — uniting Richey May, WSRP, MKA, Sobul Primes & Schenkel, and the Doty Group under F3 Partners’ backing — illustrates how platform formation itself is accelerating.

Pre-deal, Richey May sat at No. 102 on the IPA Top 200 with $57.7 million in revenue. Post-deal, the combined entity vaulted into the Top 50. Koltin projected it would reach the Top 25. The Richey May model — simultaneous multi-firm combination rather than sequential tuck-in — collapses years of traditional M&A into a single closing date and produces instant scale, which is precisely what PE sponsors prize in an environment where organic growth in accounting remains stubbornly slow, and the talent pipeline remains stubbornly narrow.

What to Expect in 2026

Phil Whitman, CEO of Whitman Advisory, predicts “2026 is going to be the year of the tuck-in.”

Whitman sees another layer of concentration: Dominant platforms are not just buying independent firms, they are buying firms that are themselves rolling up smaller practices, creating a fractal of consolidation within consolidation.

Bob Lewis, president of the Visionary Group, is more emphatic. “This is not going away,” he says. “Let it soak in: I’ve got to change how I play this entire game.”

Then came Tuesday, March 25, 2026, a single date on the tracker that logged two transactions with more structural significance than any dozen tuck-ins.

The first was Threadline Wealth. Justin Fisher, who spent 19 years at Moss Adams and led its private clients practice, carved out the firm’s wealth management division as a standalone registered investment advisor backed by the Cynosure Group, a family-office-backed alternative asset manager based in Salt Lake City and New York. Threadline launched with $5.8 billion in client assets under management, 60 employees — roughly half of them advisors — and offices in Seattle, Portland, San Francisco, and Los Angeles.

Capital Flows Reverse

The direction of capital was inverted. A CPA firm was not being acquired into the PE ecosystem. Instead, it was shedding an asset into it.

Baker Tilly, which completed its merger with Moss Adams in June 2025 in a deal valued at approximately $7 billion and backed by Hellman & Friedman and Valeas Capital, effectively let the wealth practice go, with CEO Eric Miles offering polite wishes for “continued success.”

“We really recognized that we’ve got to be all in on wealth management from an operating model and from a technology standpoint in order to really serve those clients differently in three, four years from now,” Fisher tells WealthManagement.com.

Fisher cites regulatory friction — a wealth management arm operating inside an accounting firm encounters audit-independence conflicts when it wants to invest client funds in companies the parent firm audits — and what amounts to a capital-allocation mismatch because accounting firms and wealth advisory businesses require different regulatory frameworks, technology stacks, and growth capital.

PE-Adjacent Portfolio Holdings

Cynosure, whose managing director, Keith Taylor, is a former Carlyle Group partner, already backs Steward Partners and Savant Wealth Management, which together oversee roughly $44 billion in client assets. Threadline is not an orphan. It is joining a curated portfolio of PE-adjacent wealth platforms.

The irony is palpable. The Moss Adams wealth team spent 25 years building its practice inside an accounting firm and is now better capitalized, better positioned, and arguably better served by leaving it.

The second March 25 transaction carried even deeper structural implications.

EisnerAmper and TowerBrook Capital Partners reported the completion of a continuation vehicle — a purpose-built fund structure that transferred TowerBrook’s stake in EisnerAmper from its legacy Fund V into a new vehicle, with Carlyle AlpInvest as the lead investor and Hamilton Lane as a co-lead.

TowerBrook is not exiting. It is not flipping. It is refinancing.

Moelis served as lead financial advisor, Deutsche Bank as co-lead, Kirkland & Ellis as legal counsel to TowerBrook, and Dechert as legal counsel to EisnerAmper.

The deal was described officially as “a significant realization event for TowerBrook Fund V” — language that, in private equity, means investors in that fund are getting their money back while TowerBrook rolls its economics forward with fresh institutional capital.

Continuation vehicles are standard infrastructure in mainstream buyouts. Their dollar value across all PE strategies grew from roughly $35 billion in 2019 to an estimated $100 billion or more by the end of 2025, according to Evercore. Nearly 75 percent of the largest global PE firms have now executed at least one continuation transaction, per Jefferies’ 2025 secondary market review. In 2025, GP-led secondaries, of which continuation vehicles are the dominant form, totaled $115 billion — roughly 43 percent of the entire secondary market.

But in accounting, the EisnerAmper transaction is the first. The profession has not yet fully absorbed the fact that the PE-accounting thesis is now old enough, and the underlying assets seasoned enough, that institutional secondaries investors — the Carlyle AlpInvests and Hamilton Lanes of the world, whose entire business is pricing mature private equity portfolios — are willing to underwrite them.

Not a Flip. Something Bigger.

Koltin, characteristically, captures both the surprise and its meaning. “The market was expecting to hear news of a ‘flip’ to another PE firm,” he says, “but TowerBrook surprised us with their continuation fund and simply felt the best days were yet to come for EisnerAmper.”

He adds a detail that reframes the competitive landscape. “EisnerAmper was a big beneficiary of the phrase, ‘Early adopters have their privileges,’ as many of their M&A deals came during 2022 to 2024 when there were only a handful of PE/CPA firm platforms in existence. Today, the playing field has become much more competitive for deals.”

The numbers tie out.

EisnerAmper counts 27 acquisitions since TowerBrook’s entry in July 2021, growing revenue from approximately $542 million to more than $1.2 billion and climbing to No. 13 on Accounting Today’s 2026 Top 100 list. It now fields 475 partners and 4,700 professionals across 43 offices with a presence in nine countries.

The continuation vehicle allows TowerBrook to keep compounding that growth rather than crystallize gains at what, by any measure, would already have been a spectacular exit.

The Momentum of Big Money

Charly Weinstein, CEO of Eisner Advisory Group, calls the partnership “transformational.” Walter Weil, TowerBrook’s managing director on the deal, says: “The long-term opportunity continues to be as robust as ever.”

Lewis, the Visionary Group president, assessed the EisnerAmper transaction as “the next logical step in the progression of modernizing the capital structure of the accounting profession” and calls it “proof that the trend in investing into firms has been successful enough to keep capital groups interested in further expansion into the industry.”

Lewis’s language — “modernizing the capital structure” — is doing heavy lifting. What Lewis is describing, without quite saying it, is that accounting firms are now being treated like any other private-equity-owned business: acquired, scaled, recapitalized, and repriced through institutional secondary markets.

The Trophy Life

The CFA Institute, in a 2025 report on continuation vehicles, notes that CVs “have accomplished a remarkable transformation in reputation, from an association with ‘zombie funds’ to a perceived repository of trophy assets.”

EisnerAmper, the first accounting firm to enter this secondary pipeline, is being classified as a trophy.

The contrast with the only prior secondary-market event in accounting is instructive. In January 2025, New Mountain Capital flipped its stake in Citrin Cooperman to Blackstone at a reported valuation of approximately $2 billion — up from roughly $500 million when New Mountain invested in late 2021. That was a clean sponsor-to-sponsor sale. One PE firm out, another in.

But the EisnerAmper deal is structurally different. TowerBrook stays, the fund changes, and new institutional capital enters at a valuation that, while undisclosed, is rich enough to attract two of the world’s largest secondaries investors.

More in the Pipeline

2026 may be known as the year of the flip. There are reportedly four additional transactions in the pipeline — one involving a top-50 accounting firm, another a top-100 firm, a third a top-50 rollup, and a fourth a top-100 rollup.

TowerBrook’s decision to choose a continuation vehicle rather than a flip suggests that the smartest money in accounting PE is in no hurry to exit.

CPA Trendlines’ own analytical framework identifies two parallel trends: deliberate, high-stakes moves at the top of the market and fast-paced aggregation in the middle. The Threadline and EisnerAmper transactions of March 25 add a third: capital recycling that neither enters nor exits the PE ecosystem but reshuffles within it, creating layers of institutional ownership that did not exist 18 months ago.

Mega-firms like Baker Tilly, backed by Hellman & Friedman at a $7 billion valuation, are shedding noncore divisions into PE-adjacent vehicles. Mature PE-backed platforms like EisnerAmper are refinancing into continuation structures. New platforms like Crete, Sorren, and Ascend are acquiring at a pace that, if current trajectories hold, will push several of them past $500 million in revenue within two years.

25 Years Later

Shamis, the skeptic, draws a pointed historical parallel, reminding the profession that American Express and H&R Block both tried to roll up accounting firms in the 1990s and failed.

“Are we smarter than we were 25 years ago?” Shamis wonders aloud. “We’ll find out.”

Koltin, the optimist, points to insurance brokerage, where firms are already “on their second, third, fourth, fifth flip” and the model has worked over multiple decades.

The difference between those two analogies may come down to a single word: concentration.

Insurance brokerage’s PE consolidation has produced a market in which 45 institutional buyers are consolidating roughly 35,000 independent agencies, and the threshold revenue to rank as the 100th-largest broker has jumped by more than $4 million in just four years.

Accounting, with 50-odd PE platforms chasing roughly 40,000 firms, is tracking toward the same endgame — except that its top five platforms already control 28 percent of verified deal flow, a concentration level that insurance took a decade to reach.

Regulators, What Regulators?

Meanwhile, the profession’s regulatory apparatus is scrambling to catch up.

The AICPA is seeking feedback on proposed independence-rule updates prompted by PE structures. NASBA’s PE Task Force is studying the implications of outside investment in CPA firms. Individual states are examining how alternative practice structures — the legal mechanism that splits attest services from non-attest advisory work and allows PE capital into the latter — interact with existing licensing requirements.

None of this scrutiny is slowing the deal pipeline.

When TowerBrook’s EisnerAmper deal closed, it was called “a great lab experiment.” Four years and more than 400 transactions later, the experiment has produced results that institutional secondaries investors consider investment-grade.

A Big Tuesday in March

Two deals on a single Tuesday in late March do not, by themselves, reshape a $146 billion sector.

But the Threadline spinoff and the EisnerAmper continuation vehicle, logged side by side on March 25, 2026, mark the moment when capital in PE-backed accounting stopped moving in one direction.

Money is no longer simply flowing into CPA firms from private equity. It is flowing out of CPA firms into PE-adjacent wealth vehicles, recycling between fund structures through institutional secondaries, and compounding inside platforms that their sponsors have no intention of selling.

The conventional story was that PE is coming for every CPA firm. The more accurate counter-conventional story, written in 155 deals across six platforms, may be that PE came for the firms it wanted, got them, and is now building the financial infrastructure to keep them forever.

CPA Trendlines Research Deal Tracker™

Selected Month-by-Month Deals and Analysis

March 2026

- MSTiller (MST) (Duluth, GA) acquired by Armanino (Further Global Capital Management). Announced March 2, 2026.

- Hucke and Associates (New York, NY) acquired by Ryan LLC (Neuberger Berman, Onex Partners, Ares Management). Announced March 4, 2026.

- CFO Hub LLC (San Diego, CA) joins CRI (Carr, Riggs & Ingram) (Centerbridge Partners/Bessemer Venture Partners). Effective March 5, 2026.

- Berman Hopkins CPAs & Associates (Orlando, FL) acquired by Doeren Mayhew (Audax Private Equity). Announced March 12, 2026.

- Price, Reuben, and Associates (Calabasas, CA) acquired by EisnerAmper (TowerBrook Capital Partners). Announced March 17, 2026.

- Accounting Specialists/ASG Advisors (Boca Raton, FL) joins Platform Accounting Group (The Cynosure Group). Announced March 17, 2026.

- SD Mayer & Associates (San Francisco, CA) acquired by Springline Advisory (Trinity Hunt Partners). Announced March 19, 2026.

- CG Advisory (Tinton Falls, NJ) acquired by Springline Advisory (Trinity Hunt Partners). Announced March 24, 2026.

- EisnerAmper continuation vehicle: Carlyle AlpInvest and Hamilton Lane join as new investors in EisnerAmper’s TowerBrook-backed platform. Announced March 25, 2026.

- Threadline Wealth (Seattle, WA), a wealth management spinoff from Moss Adams, announces strategic partnership with The Cynosure Group. Announced March 25, 2026.

As the first quarter concludes, the narrative is no longer just about who is buying whom, but about which investment philosophy—and which technology stack—will dominate the next decade.

1. EisnerAmper: The Institutional Standard-Bearer.

While Citrin Cooperman led 2025, March 2026 belongs to EisnerAmper. The announcement of their Continuation Vehicle—bringing in heavyweights Carlyle AlpInvest and Hamilton Lane alongside TowerBrook—is a watershed moment. This isn’t just a refinancing; it is the creation of a “permanent capital” model that moves the firm beyond the typical five-year PE exit clock. By also tucking in Price, Reuben, and Associates this month, they are proving that their appetite for high-net-worth Southern California tax practices remains unsated. They are now the “Blue Chip” platform for partners seeking long-term stability over a quick flip.

2. Springline Advisory: The Mid-Market Multiplier.

Trinity Hunt Partners’ Springline Advisory has emerged this March as the fastest-moving “New Power” in the rankings. By executing a sophisticated “coastal bookend” strategy—acquiring SD Mayer & Associates in San Francisco and CG Advisory in New Jersey within a five-day window—Springline has leapfrogged older platforms in geographic density. Their focus is surgical: they are targeting the $20M–$60M “sweet spot” firms that are too large for local players but want more personalized integration than the “Big 4-style” platforms offer. Springline is effectively building a national boutique network at scale.

3. Armanino & Further Global: The Scale Specialist.

Following the acquisition of MSTiller (MST) in early March, Armanino (backed by Further Global) has solidified its position as the premier “Sunbelt” consolidator. With MST providing a massive professional engine in the Atlanta corridor, Armanino is leveraging its “Tech-First” reputation to win over Georgia-based firms wary of traditional New York-centric roll-ups. They are differentiating themselves by not just buying revenue, but by deploying a proprietary digital transformation office into every firm they acquire, instantly upgrading legacy tax practices into high-margin advisory machines.

The Strategic Shift: AI and the “Value-Added” Professional

For professionals in the CAS (Client Advisory Services) and AI space, the March data confirms a critical trend: the “Commodity Tax” era is coming to an end.

- The “Advisory Alpha”: Every deal this month—from CRI’s acquisition of CFO Hub to Doeren Mayhew’s move for Berman Hopkins—had a heavy emphasis on non-compliance revenue. The platforms are no longer valuing firms based on their audit books, but on their ability to provide “Fractional C-Suite” services.

- Platform-Wide AI Integration: We are seeing the rise of the “Universal Data Layer.” Platforms like Platform Accounting Group (which added ASG Advisors this month) are moving toward a centralized data warehouse. This allows them to run AI-driven benchmarking across their entire portfolio of thousands of small-business clients, providing insights that a standalone $10M firm could never generate.

- The Talent War: The “Head of AI” is now a standard C-suite role in these PE-backed entities. The mandate is clear: automate the 1040/1120 production cycle to free up senior talent for the high-stakes M&A and estate planning work that justifies the massive valuations being paid by Blackstone, TowerBrook, and Trinity Hunt.

February 2026

- 1RDG (Rochester, NY) acquired by Doeren Mayhew (Audax). Announced Feb. 3, 2026.

- Meritax Advisors (Frisco, TX) acquired by Ryan LLC (Ares Management; Neuberger Berman; Onex). Announced Feb. 5, 2026. Expands Ryan’s property tax valuation strategy and litigation management.

- Williams Young McKaig Ltd (WYM Rating) (Edinburgh, UK) acquired by Ryan LLC (Ares Management; Neuberger Berman; Onex). Announced Feb. 5, 2026. Expands Ryan’s UK business rates and property tax capabilities.

- Bowers Advisors (Syracuse, NY) acquired by Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Feb. 5, 2026.

- Step Up Consulting (Los Angeles, CA; $14 million est. revenue) acquired by Armanino (Further Global Capital Management). Announced Feb. 5, 2026.

- Affiniax Group (Dubai, UAE) acquired by KNAV Advisory (Nikhil Kamath). Announced Feb. 5, 2026.

- Wagner Kaplan Duys & Wood LLP (WKDW) (Englewood, CO) acquired by Richey May (F3 Partners). Announced Feb. 9, 2026.

- Liptz & Associates (Bellingham, WA) acquired by Larson Gross, a Crete Professionals Alliance platform firm (Thrive Capital/Bessemer Venture Partners). Announced Feb. 10, 2026.

- Browne Consulting Group LLC (Boston, MA) acquired by Citrin Cooperman (Blackstone). Announced Feb. 10, 2026. Deepens Citrin’s life sciences and biotech bench.

- Peltier, Gustafson & Miller (Albuquerque, NM) acquired by Capstone Accounting and Tax (Seaside Equity Partners). Announced Feb. 11, 2026.

- Thompson Palmer & Associates (Jackson, WY; two partners, eight staff) merges into McGee, Hearne & Paiz (MHP) (Ascend/Alpine Investors). Announced Feb. 12, 2026.

- Gonzalez Advisors (Irvine, CA) acquired by Elevate Platform. Announced Feb. 18, 2026.

- Richardson Kontogouris Emerson LLP (Los Angeles, CA) acquired by Cherry Bekaert (Parthenon Capital). Announced Feb. 18, 2026.

- Smeriglio Associates/Green Coast Advisors (Greenwich, CT) joins Platform Accounting Group (The Cynosure Group). Announced Feb. 19, 2026.

- CMJ LLP (Queensbury, NY) acquired by UHY (Summit Partners). Announced Feb. 20, 2026.

- Dent Moses (Birmingham, AL) acquired by Doeren Mayhew (Audax). Announced Feb. 23, 2026.

- Impact Technology Group (Birmingham, AL) acquired by Doeren Mayhew (Audax). Announced Feb. 23, 2026.

- Larson Tax Partners (St. Louis, MO) acquired by UHY (Summit Partners). Announced Feb. 25, 2026.

- Connected Accounting (CA) joins Sorren (DFW Capital). Announced Feb. 25, 2026.

February 2026 marked a decisive shift in the “Platform Wars,” characterized by massive geographic land grabs and the emergence of specialized “sub-platforms.” While 2025 was about testing the waters, February’s deal flow proves that private equity is now moving with a “winner-take-all” urgency, specifically targeting firms that bridge the gap between traditional audit and high-margin specialized advisory.

Aprio (backed by Charlesbank) executed the most aggressive maneuver of the month, effectively colonizing the Pacific Northwest by absorbing both Delap LLP and Hoffman, Stewart & Schmidt. This “double-tap” acquisition instantly transforms Aprio into a coast-to-coast powerhouse, signaling that regional dominance is no longer enough; the top-tier PE platforms are now playing for total national coverage in high-growth tech and middle-market corridors.

The mid-market also saw heavy consolidation as established platforms refined their service portfolios. Citrin Cooperman (Blackstone) deepened its life sciences and biotech bench with the acquisition of Browne Consulting Group, while Doeren Mayhew (Audax) and UHY (Summit Partners) continued their steady roll-up of regional anchors like Dent Moses and CMJ LLP. These aren’t just volume plays; they are strategic “tuck-ins” designed to layer sophisticated tax and M&A capabilities over stable, local compliance bases.

Perhaps most significant was the formal entry of the Nichols Cauley platform, backed by Madison Dearborn Partners. Led by former Baker Tilly CEO Alan Whitman, this launch introduces a “triple-threat” model—integrating CPA, Insurance, and Transaction Advisory from day one. It serves as a reminder that the “Post-Consolidation” era isn’t just about bigger firms, but about fundamentally different firm architectures designed to scale at a pace traditional partnerships simply cannot match.

Here is the revised January 2026 section — 31 deal entries covering all 33 tracker rows (Scheidel/Sierra combined into one entry, Barb & McDowell combined into one):

January 2026

- Topping Kessler & Company (Hollywood, FL) joins PKF O’Connor Davies (Investcorp/PSP Investments). Announced Jan. 13, 2026. Expands the platform’s South Florida footprint.

- TaxOps SALT (Denver) joins Aprio effective Jan. 9, 2026. The nine-person state and local tax team is led by Judy Vorndran. (Charlesbank Capital Partners)

- Tarsus (Washington, D.C., with offices in California and Missouri; outsourced accounting and CFO advisory services) acquired by Cherry Bekaert (Parthenon Capital). Announced Jan. 13, 2026. Bolsters Cherry Bekaert’s outsourced accounting and CFO advisory practice.

- Smith Schafer (Rochester, MN) acquired by CohnReznick (Apax Partners). Effective Jan. 1, 2026. Marks CohnReznick’s entry into Minnesota.

- Scheidel, Sullivan & Lanni CPA LLC and Sierra Financial Advisors (Sacramento, CA) acquired by SAX LLP and SAX Wealth Advisors, respectively (Cobepa). Announced Jan. 7–8, 2026. SAX’s first transactions of the month.

- Sales Tax Defense (Deer Park, NY) acquired by Armanino (Further Global Capital Management). Announced Jan. 6, 2026.

- Ryan LLC (Jan. 14, 2026) reports Neuberger Berman Capital Solutions and Neuberger Berman Private Markets commit to acquire a “significant minority equity interest” for up to $1.2 billion, valuing Ryan at $7 billion. Neuberger joins Onex Partners and Ares Private Equity as minority shareholders. Closing expected in the first half of 2026.

- Rochester Tax Team (Rochester, NY) joins Modern Wealth Management (Crestview). Announced Jan. 20, 2026. Modern Wealth acquired the team from Manning & Associates.

- Riibner and Associates (Kensington, MD) joins Platform Accounting Group (The Cynosure Group). Announced Jan. 14, 2026.

- Poterack Capital Advisory (Jackson, WY; approximately $265 million in client assets) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Jan. 7, 2026.

- Owen J. Flanagan & Co. acquired by SAX LLP (Cobepa). Announced Jan. 22, 2026. SAX’s second deal of the month.

- Nichols Cauley (Dublin, GA), Partners Risk Services (Johns Creek, GA), and JGH Consulting (Atlanta) merged Jan. 5 to form a new financial services platform backed by Madison Dearborn Partners, with former Baker Tilly CEO Alan Whitman as CEO. The three-way combination launches a CPA, insurance, and transaction advisory firm from day one.

- MLCworks (New Orleans, LA) joins EisnerAmper (TowerBrook). Announced Jan. 15, 2026. Adds digital growth advisory capabilities.

- Manley Garvin (Greenwood, S.C.) acquired by UHY (Summit Partners). Effective Jan. 1, 2026. UHY’s entry into South Carolina.

- Long Run Wealth Advisors (Lake Placid, NY; approximately $640 million in client assets) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Jan. 7, 2026.

- Lancaster & Reed (Key Biscayne, FL) acquired by Doeren Mayhew (Audax). Announced Jan. 7, 2026. Establishes Doeren’s Miami international private client practice.

- Hoffman Stewart & Schmidt (Lake Oswego, Ore.) combined with Aprio effective Jan. 1, 2026, deepening the platform’s new Oregon footprint. (Charlesbank Capital Partners)

- Hess & Rohmer (Gainesville, TX) joins Sorren (DFW Capital). Announced Jan. 28, 2026. Adds to Sorren’s Texas presence.

- Herbein Financial (Reading, PA) acquired by Choreo (Parthenon Capital). Announced Jan. 21, 2026. The CPA arm — Herbein + Company — was previously acquired by Cherry Bekaert.

- Grunden Financial Advisory (Denton, TX) acquired by Allworth Financial (Lightyear Capital/Ontario Teachers’ Pension Plan). Announced Jan. 20, 2026.

- Gollob Morgan Peddy (Tyler, TX) joins Ascend (Alpine Investors). Announced Jan. 5, 2026. Adds $17 million in revenue and a strong East Texas presence.

- Gettleson Witzer & O’Connor (GWO) (Encino, CA) joins Ascend (Alpine Investors). Announced Jan. 20, 2026. Merged into the Lucas Horsfall platform firm. GWO is a family services and business management practice with a decades-long entertainment-industry client base in the San Fernando Valley.

- FSA Wealth (Needham, MA) acquired by Allworth Financial (Lightyear Capital). Closed Dec. 1, 2025; team relocated to Allworth’s Needham office. Announced Jan. 15, 2026.

- Delap (Lake Oswego, Ore.) merged into Aprio effective Jan. 1, 2026, giving Aprio its first Pacific Northwest presence. (Charlesbank Capital Partners)

- Darnell Sikes Wealth Partners (Lafayette, LA; approximately $1.9 billion in assets under management; affiliated with Darnall Sikes & Frederick CPAs) joins Avantax, a unit of Cetera Financial Group (Genstar Capital). Announced Jan. 22, 2026.

- Bradshaw Rogers (Salisbury, NC) acquired by Prime Capital (Abry Partners). Announced Jan. 22, 2026. Adds roughly $600 million AUM.

- Bowman & Company LLP (Voorhees, NJ) acquired by PKF O’Connor Davies (Investcorp/PSP Investments). Announced Jan. 5, 2026.

- Bauknight Pietras & Stormer, P.A. (Columbia, S.C.) acquired by Smith + Howard (Broad Sky Partners). Announced Jan. 13, 2026. Expands Smith + Howard into South Carolina.

- Baseline Wealth Management (London, UK) acquired by Creative Planning (TPG Capital). Announced Jan. 13, 2026. Creative Planning’s first foreign deal.

- Barb & Company and McDowell-Pearman (both Columbia, S.C.) acquired by Reid Advisors, a Crete Professionals Alliance platform firm (Thrive Capital/Bessemer Venture Partners). Announced Jan. 27, 2026. Crete’s first South Carolina presence via tuck-in.

- Alexander Almand & Bangs (AAB) (Arlington, VA) merges effective Jan. 1, 2026 with Wilson Lewis, strengthening Ascend’s Southeast footprint. (Alpine Investors)

The flurry of deals in early 2026 has officially moved the accounting industry into a “Post-Consolidation” era. The traditional “Top 100” rankings are being rewritten as private equity-backed platforms aggressively scale.

1. Citrin Cooperman: The Valuation Leader. Citrin remains among the heavyweights of the PE-backed world. Following a 2025 deal with Blackstone, Citrin has moved beyond simply acquiring firms toward building a corporate enterprise model. The firm dominates the Mid-Atlantic and Northeast corridor and is using Blackstone capital to target the West Coast.

2. Aprio: The Technological Aggressor. Aprio’s pro-forma revenue grew substantially in January 2026 following the HSS and Delap combinations in the Pacific Northwest. By targeting firms with strong PCAOB and cybersecurity practices, Aprio is positioning itself to compete for high-growth tech clients. Its entry into the Oregon/Washington corridor makes it a significant coast-to-coast PE platform.

3. Ascend: The Identity Preserver. Ascend is among the most distinctive players. Unlike Aprio or Citrin, Ascend allows acquired firms such as Gettleson Witzer (GWO) and Alexander Almand & Bangs to maintain their local identities. Ascend is capturing the “independence-minded” segment of the market, winning deals from partners at $15M–$50M firms wary of being absorbed into a national brand.

For professionals in the CAS (Client Advisory Services) and AI space, these deals are significant because they represent a massive shift in how services are delivered. All three platforms are actively standardizing their advisory offerings around AI-enabled workflows. Aprio, for instance, is moving toward a model in which human-supervised AI handles bookkeeping, allowing advisory teams to focus on strategic tax and M&A planning.

December 2025

- Sweeney Conrad (Kirkland, WA) joins Ascend (Alpine Investors). Effective Dec. 1, 2025. Adds a presence in the Seattle metropolitan market.

- Gerald Stinnett CPA PC (Suwanee, GA) joins Doeren Mayhew (Audax). Effective Dec. 1, 2025. Doeren’s second deal in the Atlanta market, following AGL CPA Group in Duluth, GA, in July. Founder Gerald Stinnett and team transition to Doeren Mayhew’s Metro Atlanta office.

- Casey Neilon (Carson City, NV) acquired by Sorren (DFW Capital). Announced Dec. 1, 2025. Establishes Sorren’s presence in Nevada. Effective October 2025, Nicola “Niki” Neilon was appointed Chair of NASBA, leading the association’s board and guiding policy on CPA licensure, mobility, and related regulatory issues across the 55 U.S. jurisdictions.

- Berkowitz Pollack Brant (BPB) (Miami, FL) — two transactions. BPB’s wealth management practice joined Baker Tilly (Hellman & Friedman) effective Dec. 1, 2025. A second BPB transaction closed Dec. 15, 2025, further expanding Baker Tilly’s South Florida footprint.

- Wolf Maryles & Associates (New York, NY) acquired by PKF O’Connor Davies (Investcorp/PSP Investments). Announced Dec. 2, 2025. Team joined the New York office effective Jan. 1, 2026.

- Burt Wealth Advisors (North Bethesda, MD) acquired by Creative Planning (TPG Capital). Announced Dec. 2, 2025. Adds approximately $1 billion AUM and establishes a North Bethesda hub.

- Glass Jacobson Wealth Advisors (Baltimore, MD) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Dec. 2, 2025. Adds approximately $1 billion AUM and deepens Mid-Atlantic presence.

- DK Partners (Austin, TX) acquired by Carr, Riggs & Ingram (Centerbridge Partners/Bessemer Venture Partners). Joined Dec. 3, 2025. CRI’s fifth merger since receiving PE funding in late 2024.

- The Vroman Group (West Des Moines, IA) acquired by BGM (Unity Partners). Announced Dec. 3, 2025.

- Marshall Financial Group (Doylestown, PA) acquired by Creative Planning (TPG Capital). Announced Dec. 9, 2025. Adds $900 million-plus AUM to the platform.

- Farkouh Furman & Faccio (New York, NY) acquired by Prosperity Partners (Unity Partners). Completed Dec. 9, 2025. Serves as Prosperity’s flagship New York City office.

- Mark Rule & Co. (Butte, MT) acquired by Capstone Accounting & Tax (Seaside Equity Partners). Joined Dec. 10, 2025. Expands Capstone into the Montana market.

- Brown and Bakondi (Oregon City, OR) and Watters and Associates (Roseburg, OR) both join Platform Accounting Group (The Cynosure Group). Announced Dec. 11, 2025. Two Oregon additions in a single day.

- RTO & Company (The Dalles, OR) joins Sorren (DFW Capital). Announced Dec. 15, 2025.

- Seghetti Waxler/Bayshore Advisors (Santa Cruz, CA) and Wayne Long & Co./Longview Advisors (Bakersfield, CA) both join Platform Accounting Group (The Cynosure Group). Announced Dec. 24, 2025. PAG closed four deals in December alone.

- North Star (Snohomish, WA) acquired by Capstone Accounting & Tax (Seaside Equity Partners). Joined Dec. 29, 2025. Strengthens Capstone’s Washington state presence.

- Geographic Land Grab: Florida and the Mid-Atlantic (Maryland/DC) were the primary battlegrounds in December, with major players like Baker Tilly, Creative Planning, and Mercer Advisors aggressively acquiring local market leaders.

- Wealth + Accounting Synergy: Firms like Mercer and Creative Planning are increasingly targeting accounting-heavy RIAs (like Glass Jacobson Wealth) to offer “connected” tax and wealth services.

- Employee Ownership Models: Unity Partners (via Prosperity) is utilizing a “Purpose Plan” for employee ownership to differentiate its acquisition model from more traditional PE structures.

November 2025

- Mize CPAs Inc. (Topeka, KS) — including Prism Financial, which manages $1.8 billion AUM — acquired by Aprio (Charlesbank). Effective Nov. 1, 2025. Adds 20 partners and 300-plus professionals.

- BiggsKofford (Colorado Springs, CO) joins Ascend (Alpine Investors). Announced early November 2025.

- Pesta Finnie & Associates (Charlotte, NC) acquired by Frazier & Deeter (General Atlantic). Announced Nov. 4, 2025. Strengthens real estate tax and family office expertise in Charlotte.

- Smart Accountants and Infinity Globus (both Ahmedabad, India) acquired by Springline Advisory (Trinity Hunt Partners). Completed Nov. 5, 2025. Offshore delivery centers acquired directly rather than outsourced — a shift toward owning global delivery capability.

- Rosen Sapperstein & Friedlander (RS&F) (Towson, MD) joins Frazier & Deeter (General Atlantic). Announced Nov. 5, 2025. Deepens Frazier & Deeter’s Mid-Atlantic footprint.

- Gatto Pope & Walwick (San Diego, CA) acquired by Citrin Cooperman (Blackstone). Announced Nov. 6, 2025. Adds 10 partners and more than 60 professionals.

- Mennenga Tax & Financial (Madison, WI) acquired by Merit Financial Advisors (Constellation Wealth Capital). Effective Oct. 31, 2025; widely reported in early November.

- Novotny CPA Group (Grand Rapids, MI) acquired by Doeren Mayhew (Audax). Effective Nov. 10, 2025. Partners Randy Novotny and Tom Winkelman joined as principals.

- KBFM (Nashville, TN) acquired by Citrin Cooperman (New Mountain Capital). Announced Nov. 11, 2025.

- Beach Freeman Lim & Cleland (El Segundo, CA) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Nov. 12, 2025. Adds 20 tax professionals and offices in El Segundo, Irvine, and Ontario, CA.

- Accuity LLP (Honolulu, HI) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Nov. 13, 2025. Crete’s first Hawaii presence.

- TBK CPA (Houston, TX) joins Doeren Mayhew (Audax). Effective Nov. 17, 2025.

- McMurray Fox (Nashville, TN) acquired by Doeren Mayhew (Audax). Effective Nov. 17, 2025.

- BGM (Bloomington, MN) acquired by Prosperity Partners (Unity Partners). Announced Nov. 17, 2025.

- Richardson & Co (Medway, MA) joins Ascend via Walter Shuffain (Alpine Investors). Effective Nov. 20, 2025. Integrated into the Boston-area Walter Shuffain hub.

- John G. Burk (Keene, NH) joins Ascend via TSS Advisors (Alpine Investors). Effective Nov. 21, 2025. Expands TSS Advisors’ footprint across Northern New England.

Global Talent Plays: The Springline acquisition of Smart Accountants and Infinity Globus highlights a shift toward acquiring offshore delivery centers in Ahmedabad, India directly rather than outsourcing to them.

Wealth-Accounting Convergence: Acquisitions such as Prism Financial (by Aprio) and Beach Freeman Lim & Cleland (by Mercer) demonstrate that the line between high-net-worth tax work and asset management continues to blur.

October 2025

-

Shorepoint Capital Partners (Norwood, MA; $850 million AUM) acquired by Allworth Financial (Lightyear Capital/Ontario Teachers’ Pension Plan). Effective Oct. 1, 2025.

-

Singer Burke (Los Angeles, CA; $1.2 billion AUM) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners) and integrated into Mercer’s ultra-high-net-worth Regis Group. Announced Oct. 7, 2025.

-

Herbein + Company (Reading, PA) acquired by Cherry Bekaert (Parthenon Capital). Announced Oct. 8, 2025. Note: Herbein’s affiliated wealth management practice — Herbein Financial — was separately acquired by Choreo in January 2026.

-

AVL Growth Partners (Boulder, CO) acquired by Ampleo (Unity Partners). Announced Oct. 15, 2025.

-

TKR Advisors (Arlington, VA) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Oct. 22, 2025.

-

Nissen & Meyer (Redmond, OR) acquired by Capstone Accounting and Tax (Seaside Equity Partners). Announced Oct. 23, 2025. Expands Capstone’s Central Oregon presence.

-

Healthworks (Los Angeles, CA) joins Sorren (DFW Capital). Announced Oct. 29

- Parthenon Capital – Backing Cherry Bekaert. Since investing in Cherry Bekaert in June 2022, Parthenon has fueled over 15 acquisitions, including the Herbein + Co. deal.

- Seaside Equity Partners – Backing Capstone Accounting and Tax. Based in San Diego, Seaside focuses on “mission-critical” services in the Western U.S. They partnered with Capstone in April 2025 using a $325 million investment vehicle and directly supported Capstone’s acquisition of Nissen & Meyer in October 2025.

- Oak Hill Capital – Backing Mercer Advisors alongside Genstar Capital and Altas Partners. Oak Hill has been an ownership partner in Mercer Advisors since 2019. This backing has enabled Mercer to scale to over $69 billion in assets, facilitating large acquisitions like Singer Burke.

- Lightyear Capital – Backing Allworth Financial. Lightyear is a specialist in financial services PE and provides the capital for Allworth Financial’s aggressive “hub-and-spoke” acquisition model, which includes the Shorepoint Capital deal.

September 2025

-

Richey May (Denver, CO), WSRP (UT), Moss Krusick & Associates (Winter Park, FL), USX Advisors (Seattle, WA), and Sobul, Primes & Schenkel (CA) combined Sept. 9, 2025 to form a national platform backed by F3 Partners. Pre-deal, Richey May ranked No. 102 on the IPA Top 200 with $57.7 million in revenue. The combined entity vaulted into the Top 50.

-

Auxis (Coral Gables, FL) acquired by Grant Thornton Advisors (New Mountain Capital). Closed Sept. 2, 2025.

-

KSDT (Miami, FL) acquired by Ascend (Alpine Investors). Announced Sept. 3, 2025. Ascend’s largest merger to date at the time — adds five offices, 29 partners, and 276 professionals.

-

Horton Lee Burnett (Birmingham, AL) acquired by Smith + Howard (Broad Sky Partners). Announced Sept. 3, 2025.

-

ORBA (Ostrow Reisin Berk & Abrams) (Chicago, IL) acquired by Citrin Cooperman (Blackstone). Announced Sept. 4, 2025.

-

Mauldin Vaught (Fayetteville, AR) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Sept. 8, 2025.

-

Prism Financial (Overland Park, KS; $1.8 billion AUM) acquired by Aprio (Charlesbank). Announced Sept. 19, 2025. Note: Prism is also referenced in the Mize CPAs entry for November — verify whether these are two separate transactions or a single deal reported in stages.

-

Carson & McKinney (Nashville, TN) acquired by Doeren Mayhew (Audax). Announced Sept. 22, 2025.

-

Advisent (San Diego, CA) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Sept. 18, 2025.

- Dhruva Advisors (Mumbai, India) — Ryan LLC (Ares Management) takes a majority interest/JV stake. Announced Sept. 29, 2025. Ryan’s India market entry.

- Schulman Lobel (New York, NY) joins SAINVUS. Announced Sept. 30, 2025. SAINVUS is a founder-led family office platform, not a traditional PE-backed roll-up.