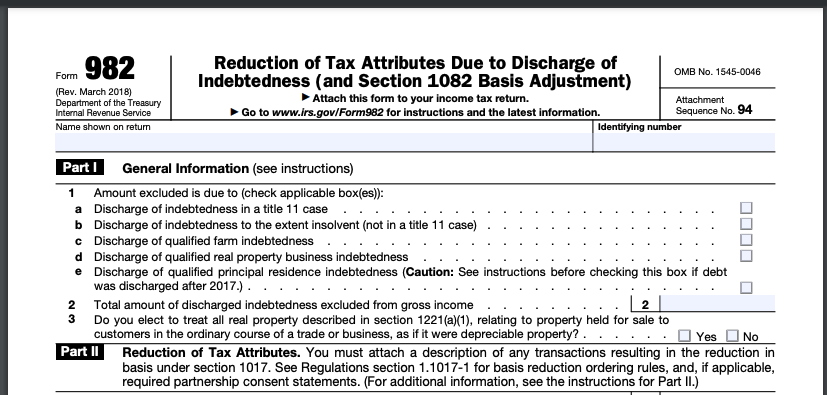

Meet Form 982.

Meet Form 982.

By Eric L. Green

Tax Rep Network

“What do you mean I have to pay tax on that debt? It was a debt, and they forgave it. The bank gave me a gift; I am pretty sure that is how it works.”

MORE: Offers in Compromise Aren’t for Everyone

Exclusively for PRO Members. Log in here or upgrade to PRO today.

All of a sudden, my client – who five minutes before told me they knew nothing about taxes – is now explaining to me, a tax attorney, that the canceled debt cannot be income and that a third-party bank obviously meant it as a gift.

Sadly, it is not a gift; there was never any intent for it to be a gift. When either the bank or another creditor writes off that debt you owed, they are required to file a 1099-C to report the canceled debt to the IRS so the lender can take the bad debt write-off. According to Congress, the courts and the IRS, the recipient now has income because they received value that they do not have to repay. In tax parlance it’s called an “ascension to wealth.”