And What 20 Years of Data Say Comes Next

By CPA Trendlines Research

There is a ritual to tax season. It begins with anticipation dressed as control.

Practitioners tally the risks — the IRS, the law, the clients who will not deliver on time — and tell themselves this year will be different. Then the season starts. And it isn’t.

MORE Busy Season Barometer | Join the survey. Get the results

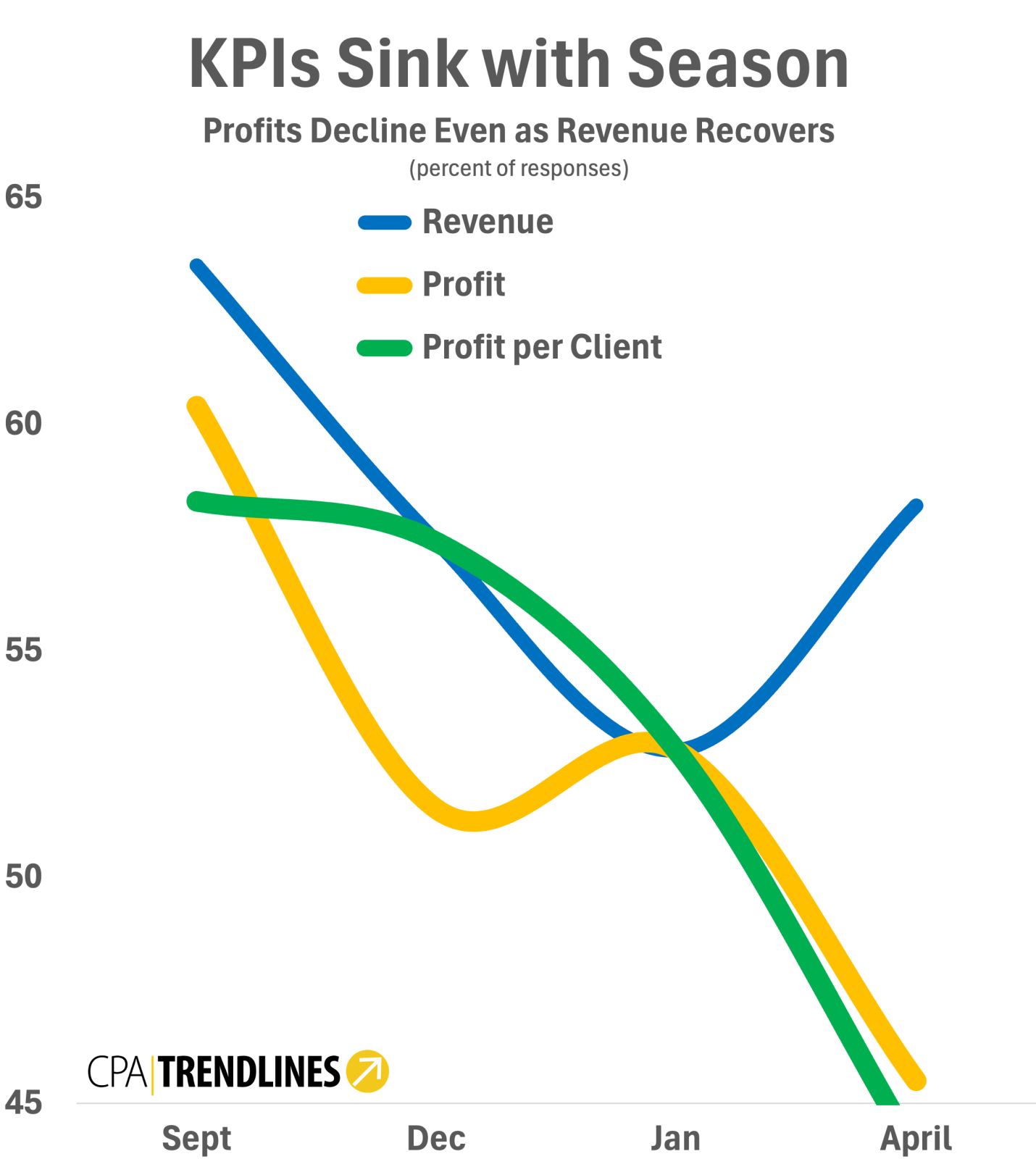

The CPA Trendlines Busy Season Barometer tracks that ritual across waves of surveys from September 2025 through April 2026 with more than 300 respondents.

The data show not a profession in crisis, but a profession under stress. Where pressures no longer arrive one at a time but stack up on each other. Where external shocks have been absorbed, and internal limits have come into view.

The data show not a profession in crisis, but a profession under stress. Where pressures no longer arrive one at a time but stack up on each other. Where external shocks have been absorbed, and internal limits have come into view.

Tax season is full of noise, chaos and confusion. But a close look at the Busy Season Barometer from this year – and going back more than 20 years – can cut through the fog for the patterns, trends, insights and, most of all, the tough lessons learned.

Tax season 2026 gives us at least 21 essential takeaways.