Venture capital crashes the private equity party in accounting.

By CPA Trendlines Research

Private equity’s push into accounting is entering a new and more complicated phase: platform building, sponsor recycling, technology investments, blended tax and wealth services — and now, a new pipeline of cash from venture capital.

MORE PE Wars: The CPA Platform Economy Is Concentrating Fast | Alan Whitman: Why the Next Big CPA Firms Won’t Look Like CPA Firms | Gear Up for Growth | The PE Takeover: Audit Problem? What Audit Problem? | 1,000 Deals Show Where PE Money in Accounting Really Goes. | The 7.6x Machine: How Grassroots Firms Are Taking Private Equity for a Ride | Deal Tracker: PE Platforms Accelerate the Grab for CPA Firms | With Apax Sale, CohnReznick Starts Building a National Platform | PE Deal Tracker for Feb. 2026: 57 deals in 60 days | PE Deal Tracker Update: Alan Whitman Plants a Flag in the Private Equity Landscape | Alan Whitman: Breaking the Mold with PE Backing | Holistic Guide

MORE Private Equity

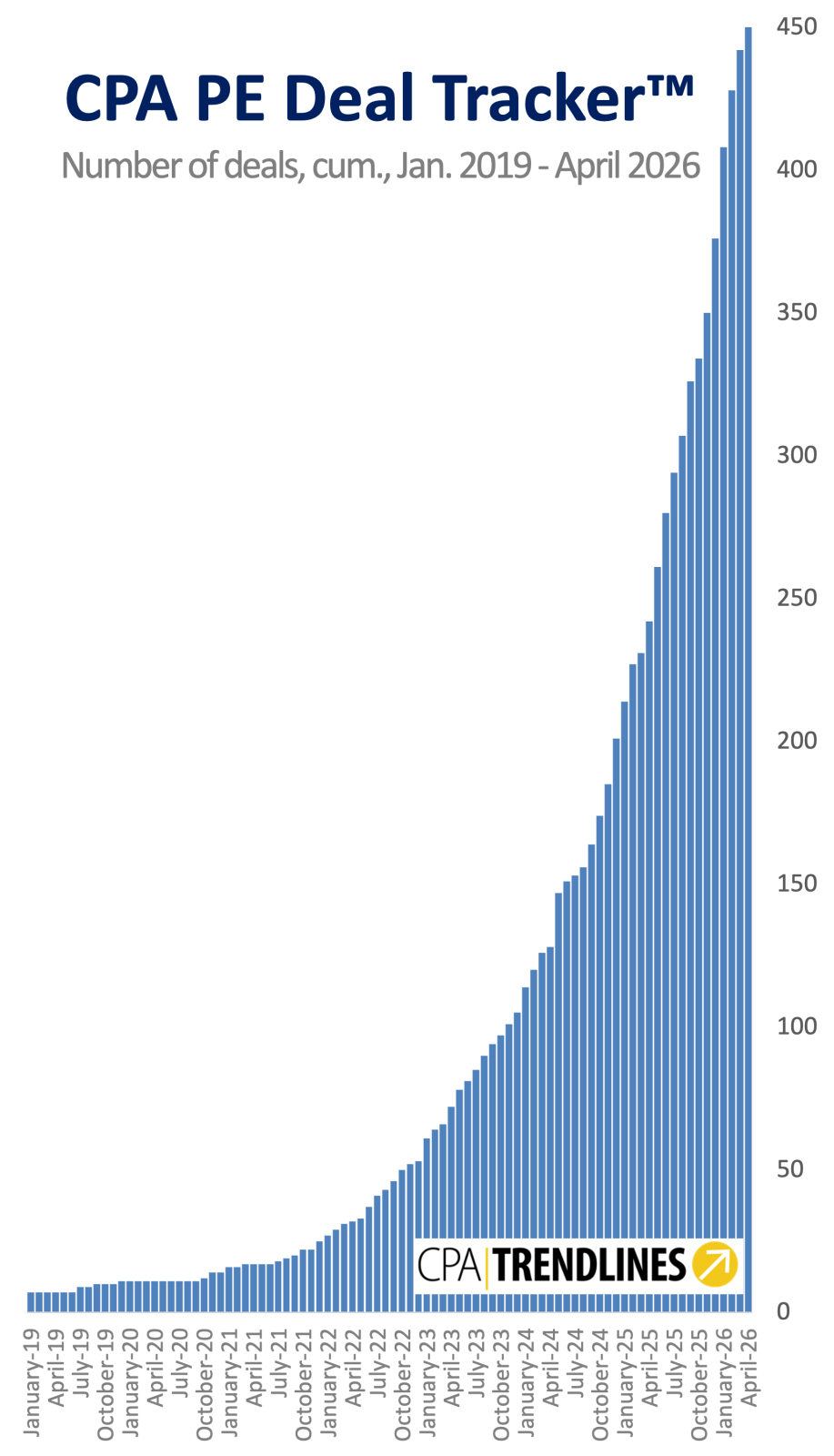

This month’s CPA Trendlines CPA-PE Deal Tracker™ shows nine new deals in April, down from the first-quarter deal-closing frenzy but bringing the year-to-date deal count through April 30 to 78, well ahead of the 44 logged in the same window of 2025.

The broader verified dataset now includes 452 in-scope events, giving CPA Trendlines a clearer view of what private capital is doing after its first wave of accounting-firm investments.

The latest data does not show a retreat. It shows a transformation. The new gambits go well beyond roll-ups, and include service line extensions, corporate carve-outs, cross-industry tie-ups, recapitalizations, continuations and a buzzy new venture-backed startup.

World domination

The deal models are sprawling in all directions as big money battles for a dwindling number of prime firms and squeezes for synergies in the firms they’ve acquired.

In the mix, accounting is morphing from a profession into a platform. A launchpad from which to sell a growing, and traditionally conflict-laden, range of products and services. From tax planning to wealth management, from outsourced accounting systems to internal audit, and from risk management to insurance sales.

A once incongruous, even contradictory, collection of services are being acquired, aligned and advanced. The ambition is market encirclement. The impulse is world domination.

Sikich: White-glove service offerings

Sikich may be the clearest example in this month’s Tracker. The Bain-backed Chicago-based firm appears twice in April, buying Burwood Group, based in Oak Brook, Ill., on April 7 and carving Milwaukee-based Jefferson Wells U.S. out of ManpowerGroup, the multinational workforce agency, on April 30.

The Jefferson Wells transaction brings Sikich more than 300 U.S. employees and $76 million in 2025 revenue in a $100 million deal. ManpowerGroup expects net cash proceeds of about $88 million at closing, after working capital and other adjustments.

Jefferson Wells adds specialized expertise in internal audit, risk and compliance, and tax technology for companies in financial services, technology and energy. With the Burwood deal, Sikich offers the second on the one-two punch: a unified business-technology-compliance stack to enterprise clients.

Sikich Chairman and CEO Christopher Geier says the Jefferson Wells deal adds “deep expertise in risk and compliance, finance and accounting, and tax” — a plain-English summary of where the acquisition market is going.

That’s no routine tuck-in. It is Sikich stockpiling skills and services.

CPA Trendlines CPA-PE Deal Tracker™ for April 2026

Target |

Platform |

Sponsor |

Event |

Category |

Strategic signal |

CAVU Advisors |

Aprio |

Charlesbank Capital Partners |

M&A |

Government contracting |

Outsourced accounting systems and federal-contractor specialization |

Burwood Group |

Sikich |

Bain Capital |

Structural |

IT consulting |

Digital transformation and enterprise technology services |

CMM, LLP |

J.S. Held |

Kelso & Company |

M&A |

Forensics and valuation |

Non-CPA consulting platform buying CPA-adjacent expert testimony capability |

GDM Private Financial Solutions |

Soltis Investment Advisors |

Estancia Capital Partners; LLR Partners |

M&A |

Wealth-tax integration |

RIA-backed buyer adding CPA-led tax capacity |

Modus (platform formation; $85M Seed + Series A) |

Modus |

Lightspeed Venture Partners; Comma Capital; Garry Tan |

Capital |

AI-native audit |

Venture-backed platform formation and audit technology thesis |

KLG Business Valuators & Forensic Accountants |

EisnerAmper |

TowerBrook Capital Partners |

M&A |

Forensics and valuation |

Litigation support, expert testimony and high-stakes dispute work |

St. Clair & Associates |

Platform Accounting Group |

The Cynosure Group |

M&A |

Regional CPA expansion |

Federated sub-brand expansion through Keystone Advisors |

CompliancePoint |

Wipfli |

New Mountain Capital |

Capital |

Cybersecurity and privacy |

Cybersecurity, privacy, compliance and regulatory advisory |

Jefferson Wells U.S. |

Sikich |

Bain Capital |

Capital |

Risk and compliance |

Risk, compliance, finance, accounting and tax technology capacity |

White-collar warehouse of white-glove services

Burwood is an IT consulting and integration firm with a nearly 30-year history serving enterprise clients in health care, higher education, industrials and financial services.

Geier says Burwood brings increased technical breadth and depth across Sikich’s technology stack. Burwood President Jim Hart says the combination brings together two brands with complementary digital transformation offerings.

Sikich’s April was the month in miniature.

Private equity-backed CPA platforms are not only buying revenue. They are buying adjacencies: technology consulting, cybersecurity, risk, compliance, tax capacity, litigation support, valuation, government contracting and AI-enabled delivery models.

The tax and accounting profession is emerging as something much more than tax and accounting. It is being recast as a central warehouse of white-collar professionals delivering white-glove strategies for wealthy families and private businesses.

Aprio: Specialization as a competitive moat

Aprio’s April 1 acquisition of CAVU Advisors shows the move toward specialization. It’s a textbook example of a top 20 firm buying an entrenched niche player to deepen its industry-specific moat.

CAVU, founded in 2005 and based in Columbia, Md., gives Aprio deeper access to the federal contracting market, where CAVU is known for outsourced accounting expertise in the high-altitude compliance needed for aerospace and defense firms.

As an elite partner for specialized ERP systems like Unanet and Deltek, CAVU runs the operating systems for government contractors. Aprio says the deal expands its ability to serve clients across accounting, tax, cybersecurity, transaction advisory, wealth and legal services.

Aprio’s aerospace, defense and government clients “need more than an accounting firm,” says CEO Richard Kopelman. “They need a partner who knows their world.”

For CPA firms, Kopelman’s take may matter more than the deal itself. It shows how industry specialization is becoming part of the PE-backed platform rationale. Firms that own a fortified niche can be more valuable than ones that bring geographic coverage or a book of recurring compliance work.

EisnerAmper: Forensics, valuation and the advisory premium

Forensics and valuation are moving in the same direction.

On April 9, New York-based EisnerAmper announces that KLG Business Valuators & Forensic Accountants, in Melville, N.Y., will join the firm, strengthening EisnerAmper’s national forensic accounting, business valuation, litigation support and expert witness testimony capabilities.

KLG, founded in 1980, works in matrimonial matters, shareholder and commercial disputes, economic damages, estate and gift tax planning, and court-appointed neutral expert work.

EisnerAmper Vice Chair of Services Christopher Loiacono says KLG has built a reputation for “credible, rigorous and trusted work” in complex valuation and forensic matters. KLG’s real asset is not just staff, but credibility in high-stakes disputes.

Forensic accounting joins the rotation

Just as PE-to-PE flips reorder ownership of CPA platforms like Citrin Cooperman and Schellman, institutional capital is consolidating the forensic accounting and dispute-advisory layer that surrounds the profession.

J.S. Held, the 50-year-old global consulting firm based in Jericho, N.Y., illustrates the pattern. Lovell Minnick Partners, a financial-services-focused private equity firm in Radnor, Pa., took control in March 2015 and built J.S. Held from a specialty consulting shop into an 18-acquisition platform with more than 600 professionals across 60 offices.

In May 2019, Kelso & Company acquired the majority stake from Lovell Minnick out of Kelso Fund X, with Harvest Partners joining as co-investor in early 2022. Under Kelso, J.S. Held has completed roughly two dozen further acquisitions, including a deliberate roll-up of forensic-accounting practices: IPFC Corp. in 2021, Ocean Tomo and AEA Group in 2022 and 2023, Phoenix Management Services and its FINRA-registered Phoenix IB broker-dealer in 2023, Forensic Resolutions in 2024, ADS Forensics and Stapleton Group later in 2024, MorrisAnderson in 2025, and CMM LLP — a New York forensic accounting and business valuation firm specializing in family-law disputes — in April 2026.

Not a “CPA” firm

Lovell Minnick, having flipped J.S. Held to Kelso, returned to the profession in October 2024 with a platform investment in Cleveland-based Cohen & Co., the IPA Top 100 firm, where it is now the sponsor of record on six tuck-ins. The firm operates the Lovell Minnick playbook on both sides of the audit and attest licensure boundary.

Every J.S. Held press release carries the disclaimer that the firm “is not a certified public accounting firm.” But the company’s impact on the profession can’t be ignored.

The most attractive CPA-adjacent practices are taking engagements that require judgment, documentation, expert testimony and specialized knowledge. Those practices are harder to commoditize than routine compliance work. They are also ripe for scaling by a national platform with brand, capital, recruiting and referral reach.

Wipfli: Redefining the “CPA” firm

Wipfli’s April 30 CompliancePoint transaction pushes the same logic into cybersecurity and regulatory risk, with two partners and 52 associates joining the firm.

Wipfli Advisory CEO Kurt Gresens says organizations are under pressure to protect sensitive information in an “evolving regulatory environment.”

Duluth, Ga.-based CompliancePoint President Greg Sparrow says Wipfli shares CompliancePoint’s commitment to practical, client-focused solutions and long-term relationships.

But this is where the old definition of a CPA firm starts to break down.

A PE-backed accounting platform can now look like a tax firm, a risk advisory shop, a cybersecurity consultant, a valuation firm, a government-contracting specialist, a wealth-tax office or a technology-enabled audit platform.

In April, PE-backed CPA firms looked like all of them at once.

Wealth management pushes into tax practice

Leaderboard: Top Ten Backers

by Number of Deals, All-time

Alpine Investors |

40 |

Ares |

24 |

TowerBrook Capital Partners |

24 |

Charlesbank Capital Partners |

24 |

The Cynosure Group |

22 |

DFW Capital Partners |

20 |

Thrive Capital; Bessemer Venture Partners |

18 |

Audax Private Equity |

18 |

Unity Partners |

13 |

Horizon Capital |

12 |

The wealth management convergence with tax practices shows up, as well, in Utah-based Soltis Investment Advisors’ acquisition of GDM Private Financial Solutions, a CPA firm in Bellevue, Wash.

Soltis, an RIA with about $13 billion of client assets, says GDM adds tax advisory to its service mix. Soltis is backed by private equity firms Estancia Capital Partners and LLR Partners, funding an aggressive expansion into integrated professional services.

Soltis CEO Clark Taylor says GDM is “a natural extension” of how Soltis serves clients, particularly as clients ask for more coordinated in-house tax strategy.

The transaction is small by headcount but large by implication. It reverses the usual buyer logic. Instead of a CPA platform adding wealth services, a PE-backed wealth platform is adding a CPA-led tax and accounting team.

For firms that have historically controlled the tax relationship, the deal signals that RIAs do not need to wait for CPA referrals if they can buy tax capacity themselves.

Platform Accounting Group: The federated-brand model

Platform Accounting Group’s April 28 addition of St. Clair & Associates, in Pottsville, Pa., looks at first like the smallest deal of the month — a one-partner, eight-staff firm that has served small businesses in central Pennsylvania for more than 50 years. By headcount, it is.

By design, it is something else.

St. Clair is not joining Platform under the Platform brand. It is joining Keystone Advisors, the Holladay, Utah-based firm Platform itself acquired in February 2025. The new combination is Platform’s second Pennsylvania location, but it sits inside a sub-brand rather than a national one.

That is a different platform model from Sikich’s stack-stitching or Aprio’s niche-deepening. The Cynosure Group-backed platform is building a federated structure in which acquired firms keep their local relationships, fold into regional sub-brands, and share back-office, technology and capital. It is closer to a holding company than a roll-up.

“We are thrilled for this next chapter as part of the Platform ecosystem,” says Bill Kirwan, principal at St. Clair. The word that matters in his sentence is “ecosystem.”

For small firm owners deciding what to do next, Platform’s federated model is a third option, neither full absorption nor independence.

Modus: Venture capital with a software thesis

Then there is Modus, the April entry that most clearly breaks the old pattern — and the most consequential of April’s nine events.

On April 7, the ten-month-old New York company closed an $85 million capital raise — $5 million in seed funding plus an $80 million Series A — led by Lightspeed Venture Partners, with participation from Comma Capital and Garry Tan, the president and chief executive of Y Combinator.

The proceeds are earmarked for taking majority stakes in advisory entities affiliated with accounting firms. Modus has already taken a position in an unidentified top-200 firm with more than $30 million in revenue. Five or more deals are expected by the end of the year.

The capital is from venture funds, not private equity. And the pitch is software, not scale.

Mix tech and accounting. Add a dash of cash. Stir.

Modus is not a traditional CPA-firm acquisition. It is an AI-native audit technology platform and holding company.

“Audits serve as the cornerstone for trust in our capital markets,” says Co-founder and CEO Arush Jain, “yet the underlying tools and workflows have not meaningfully changed in decades.”

“This funding,” Jain says, “allows us to invest aggressively in AI-enabled audit tooling while partnering with exceptional firms that want to lead the profession forward, without sacrificing quality or culture.”

The Modus deal changes the entry point for Wall Street. The first PE-backed accounting platforms began with firms and added capital. But Modus begins with technology and adds accounting. That is not merely another deal in the Tracker. It is an altogether different theory of how the business works.

Arbitrage: A different buyer profile

What separates Modus from every private equity-funded platform is what the capital is buying. PE sponsors buy existing firms and stitch them into new brands or platforms. Modus is buying the right to integrate AI-native audit infrastructure into the firms it acquires.

The founders are not accountants. They are arbitragers.

Jain and his co-founders, Pranav Pillai, the chief technology officer, and Vinay Kasat, the chief operating officer, met at the University of Pennsylvania and built careers in software before founding Modus in June 2025. The team draws on prior experience at Palantir, Citadel, Ramp, Thoma Bravo, Bridgewater and Amazon Web Services.

Modus advisers include Jim Burton, the former chief auditor at Grant Thornton, and Brian Blaha, the former chief growth officer at Wipfli, and an unnamed former chief executive of a top-10 accounting firm.

“The Modus team,” says Justin Overdorff, a partner at Lightspeed who led the firm’s investment, “has driven highly effective automation in key audit workflows and meaningfully increased efficiencies for firms performing audits.”

Two other Lightspeed partners on the deal, Isaac Kim and Amish Desai, characterize the opportunity in the language of under-service rather than disruption.

“Public accounting has been historically underserved by technology,” they say in a joint statement. “Modus intends to drive the industry forward with thoughtful product philosophy and a partnership-first approach that earns the trust of each firm they invest in.”

The one-stop shop for digital transformation

The Lightspeed framework treats audit as a domain that has been bypassed by the AI productivity revolution reshaping adjacent professional services.

“We’ve spent the last two years watching AI fundamentally shift the economics of knowledge work,” the firm says. “Capacity and the ability to serve work today is a function of people alone. To grow, you hire six months in advance and hope staff stay motivated through a grueling busy season year-over-year.”

“To us,” they say, “audit is one of the largest domains that is underserved by these advancements, but ripe to reap the benefits of them.”

Modus describes its own model in the language of partnership rather than acquisition. “Modus is a strategic acquirer of CPA firms and a technology company,” the firm says publicly. “For CPA firms — we’d like to be your long-term technology, capital, and growth partner.”

The combination is unusual in the Tracker. Private equity sponsors usually present themselves as capital partners with operational support. Software vendors present themselves as technology partners with no ownership interest. But Modus is presenting itself as both, in one package, one stop, one price.

Crete’s thesis validated

To be sure, Modus is the second venture-funded platform-formation event in the Tracker’s history.

The first, of course, is Crete Professionals Alliance, formed in May 2024, and backed by Bessemer Venture Partners and Josh Kushner’s Thrive Capital. Kushner, the younger brother of Jared Kushner, made his bones as an early Instagram backer, and today is a central figure behind ChatGPT’s OpenAI.

The arrival of Modus as a second VC-led platform ratifies Crete’s strategy, making the company look less like an experiment and more like a category.

The Tracker now lists 71 unique platforms, sponsored by 62 investors.

Until 2024 every investor in the list was a private equity firm, a long-hold growth investor or a strategic capital provider underwriting a hold-and-flip thesis.

The flavor of money

The arrival of venture capital introduces a different set of expectations. Shorter time horizons in some funds, longer in others. A tolerance for losses that PE underwriting does not share. And a belief that the operating model, not the asset base, is what will compound.

With venture capital, the competition for independent CPA firms only intensifies.

For the firm owner deciding whether to take outside capital, the question is no longer which private equity sponsor might call.

The question is, instead, what kind of capital is calling. And what the firm will be expected to look like at the end of the hold period.

Second-generation PE: platforms trade like stocks

The April Tracker, therefore, has to be read through two lenses. The first is the deal count. The second is architecture.

The deal-count story is still substantial. April was slower than January, but the Tracker shows 78 verified 2026 events through April 30, following 175 in all of 2025, still the Tracker’s high-water mark.

The April list alone includes Aprio-CAVU, J.S. Held-CMM, Modus, Sikich-Burwood, Soltis-GDM, EisnerAmper-KLG, Platform Accounting Group-St. Clair, Sikich-Jefferson Wells and Wipfli-CompliancePoint.

But the architecture story may be more important. And the 2021 cohort of accounting firms that took private equity money first — EisnerAmper, Citrin Cooperman and Schellman — is now showing what the second capital event looks like.

Schellman: A 2021 platform recapitalized

On March 5, Tampa-based Schellman, the cybersecurity compliance and attestation firm that took its first PE money from Lightyear Capital in September 2021, announced a strategic investment from Private Equity at Goldman Sachs Alternatives. Lightyear, after roughly five years as the majority investor, moves to minority. The deal is expected to close at the end of the second quarter.

“We are incredibly excited to partner with Goldman Sachs Alternatives,” Schellman CEO Avani Desai says. “From the outset, it was clear they understand our vision, our culture, and the opportunity ahead of us.”

Harsh Nanda, partner and head of technology private equity at Goldman Sachs Alternatives, frames the firm in the language of a software-like asset: “Schellman has built a category-leading, differentiated platform offering attestation and compliance services.” That is the language Wall Street uses for tech holdings, not for CPA firms.

Desai told Accounting Today that Schellman plans to use the proceeds to expand into health care and financial services, fund larger M&A deals and grow internationally, with an emphasis on Europe and the United Kingdom. The firm is No. 46 on Accounting Today’s 2026 Top 100 list, with $197 million in revenue.

Schellman is the cleanest example of the partial-flip pattern. The original sponsor stays in the cap table. A new lead sponsor takes control. The platform keeps acquiring. Nothing operational stops.

Not a “flip”

Leaderboard: Top 25 Platforms

by Number of Deals

Ryan LLC |

42 |

Ascend |

40 |

EisnerAmper |

25 |

Aprio |

24 |

Platform Accounting Group |

22 |

Sorren |

20 |

Crete Professionals Alliance |

19 |

Doeren Mayhew |

18 |

Dains LLP |

13 |

Modern Wealth Management |

11 |

Azets |

10 |

SAX Advisory Group |

10 |

Citrin Cooperman |

9 |

Cherry Bekaert |

9 |

Prosperity Partners |

9 |

Baker Tilly |

9 |

Springline Advisory |

8 |

UHY |

8 |

Cohen & Co. |

7 |

Mercer Advisors |

7 |

Capstone Accounting and Tax |

7 |

Richey May |

7 |

CBIZ Inc. |

6 |

PKF O’Connor Davies |

6 |

Armanino |

5 |

April’s deal flow shows buyers are building service stacks, industry verticals and technology-enabled delivery systems. They are not just aggregating firms. They are trying to change what the platform can sell.

The accounting profession is no longer merely watching private equity firms buy CPA firms. It is watching PE-backed accounting platforms mature into tradable, refinance-able, holdable and resale-able properties.

Citrin Cooperman, EisnerAmper and Schellman show three versions of that shift: a clean sponsor-to-sponsor transition, a continuation-vehicle transaction and a strategic investment with rollover.

But don’t use the term “flip” quite yet. It’s too imprecise for the facts.

Control changes. But deal flow doesn’t.

Even so, Citrin Cooperman fits “flip” most closely. In January 2025, Blackstone bought New Mountain Capital’s stake outright, four years after New Mountain seeded the platform in October 2021. EisnerAmper does not fit “flip” at all. Schellman sits somewhere between a sponsor transition and a rollover transaction.

The better frame is second-generation PE ownership, the stage when platforms that were first bought or backed in 2021 and 2022 start facing the next capital event.

April shows that those capital events do not stop the acquisition machine. They sit above it.

EisnerAmper illustrates the point. In March, its TowerBrook-backed continuation vehicle brought in Carlyle AlpInvest and Hamilton Lane as new investors while extending TowerBrook’s hold.

In April, EisnerAmper kept buying apace, with KLG. EisnerAmper’s capital structure may have changed, but the growth strategy continued.

That’s the inflection.

The first phase of PE in accounting asked whether outside capital could enter the profession at scale. The second phase asked how quickly PE-backed platforms could acquire firms. The current phase asks what those platforms become after capital has had time to work.

What the data does and does not show

The Tracker can identify when a new species of capital enters the profession. But it cannot yet tell whether the species will survive and replicate, or fail and wither away.

Crete remains the only VC-backed platform with a meaningful operational track record, and its trajectory — 24 deals across roughly two years, sponsor-stable, integration ongoing — is not yet an answer about whether the venture-capital thesis works in this profession. Modus has a press release and a plan.

Maybe the historical platform-formation cadence offers a comparison.

From the Tracker’s earliest entries through the end of 2020, the dataset records two initial PE-entry platform-formation events. In 2021, there were three. In 2022, four. In 2023, eight. In 2024, 11. In 2025, seven.

The pace of new platforms has not slowed. The variety of capital backing them has grown. Until April 2026, every dollar funding a new platform in the prior twelve months came from private equity, growth equity or family-office capital.

Outlier or leader?

April’s Modus round breaks that streak. There is no second VC-led platform in 2026 beyond Modus.

There is no announcement from a competing venture firm proposing a similar thesis. There is no public indication that other venture-capital sources are preparing to enter the profession at scale.

One round from Lightspeed and a YC-affiliated check is the entire data point.

So the Tracker offers two different readings.

In one, Modus is the second instance of a pattern that began with Crete and is now establishing itself. Venture capital is targeting the accounting profession as a promising sector, and additional rounds should follow.

In the other, Modus is the second of two outliers. Can the profession produce venture-style returns? Will they repeat at scale?

Big numbers

For the first time in the Tracker’s history, a CPA firm choosing to take outside capital has a non-PE option, structured around an operating thesis that no PE sponsor has financed at this price.

Today, the answer to what PE-backed accounting platforms are becoming looks less like a conventional roll-up and more like the early architecture of a new professional services model: part CPA firm, part advisory platform, part risk shop, part technology business, part stockbroker-tax integrator and part capital-market asset — a fungible financial instrument.

For CPA firms, the practical questions are no longer only “Who’s buying?” or “Who might own the firm next?”

Firms have a third question: “What flavor of capital is calling?”

And a fourth: “What will the firm be expected to look like at the end of the hold period?”

The numbers tell the story

The April Tracker racks up a lot of numbers. But the most important isn’t nine deals. Nor five acquisitions. Or three financing events. Not even one recapitalization.

It’s the bigger number: 452. Four hundred fifty-two confirmed events in a market that now has enough history to reveal patterns.

Private equity is still buying accounting firms. But it is also doing what private equity eventually does with assets it already owns: restructuring them, refinancing them, extending them and preparing them for the next owner, the next fund or the next operating model.

And starting in April 2026, so is venture capital.

The next twelve months will determine which reading the Tracker confirms. The April figure — one VC-led platform formation, $85 million in capital, AI-native operating thesis — is the data point against which the next reading will be measured.

And then came May

Early May only reinforced the picture. Alpine Investors-backed Ascend adds Jackson Thornton, the Montgomery, Ala.-based firm, lifting the Tracker’s 2026 count to 79 on May 1 and pushing Ascend’s platform deal velocity higher still.

CPA Trendlines CPA-PE Deal Tracker™

Selected Month-by-Month Deals and Analysis

April 2026

- CAVU Advisors (Columbia, MD) acquired by Aprio (Charlesbank Capital Partners). Announced April 1, 2026. Expands Aprio’s DMV government-contracting advisory practice.

- CMM, LLP (New York, NY) acquired by J.S. Held (Kelso & Company). Announced April 7, 2026. Adds forensic accounting, litigation consulting, business valuation and family law dispute work.

- Modus (platform formation; $85M Seed + Series A) (New York, NY) formed with capital backing from Modus (Lightspeed Venture Partners; Comma Capital; Garry Tan). Announced April 7, 2026.

- Burwood Group (Oak Brook, IL) acquired by Sikich (Bain Capital). Announced April 7, 2026. Adds IT consulting and digital transformation capacity.

- GDM Private Financial Solutions (Bellevue, WA) acquired by Soltis Investment Advisors (Estancia Capital Partners; LLR Partners). Announced April 7, 2026. The 11-person CPA team becomes Soltis Tax Solutions.

- KLG Business Valuators & Forensic Accountants (Melville, NY) acquired by EisnerAmper (TowerBrook Capital Partners). Announced April 9, 2026. Adds forensic accounting, business valuation and litigation support.

- St. Clair & Associates (Pottsville, PA) acquired by Platform Accounting Group (The Cynosure Group). Announced April 28, 2026. Adds a second Pennsylvania location through the Keystone Advisors hub.

- Jefferson Wells U.S. (Milwaukee, WI) acquired by Sikich (Bain Capital). Announced April 30, 2026.

- CompliancePoint (Duluth, GA) acquired by Wipfli (New Mountain Capital). Announced April 30, 2026. Adds two partners and 52 associates in cybersecurity, privacy, and compliance.

April 2026 widened the deal-tracker lens. The month produced nine events: five core M&A transactions, three capital events, and one structural event. The center of gravity shifted from ordinary regional tuck-ins toward capability acquisition: forensic accounting, federal contracting, cybersecurity, IT transformation, tax advisory inside wealth platforms, and AI-native audit infrastructure.

- Sikich: The Capability Stack Builder.

Sikich was the most active April platform, appearing twice in the month’s normalized layer. Burwood Group adds IT consulting and digital transformation, while Jefferson Wells adds a much larger risk, compliance, finance, accounting and tax services engine. The Jefferson Wells transaction is the month’s clearest scale signal: the workbook records a $100 million deal value, more than 300 U.S. employees, and $76 million in 2025 U.S. revenue.

- Forensics and Valuation Move to the Front.

EisnerAmper’s KLG combination and J.S. Held’s CMM acquisition point to the same demand curve. PE-backed platforms are not only buying tax capacity. They are buying defensible advisory niches tied to litigation, expert testimony, business valuation, family law disputes and forensic accounting. These practices carry less commodity pressure than compliance work and give platforms stronger pricing power in complex matters.

- AI-Native Audit Enters the Tracker.

Modus changes the character of the month. The workbook classifies it as a capital event, not a traditional CPA-firm acquisition, but its inclusion matters because it shows venture-backed infrastructure moving directly into the accounting platform model. The notes record $5 million in seed financing and an $80 million Series A, with a plan for majority investments in advisory entities affiliated with accounting firms.

The Strategic Shift: From Roll-Up Volume to Operating Architecture

The April data show a market that is still consolidating, but the transaction logic is becoming more technical. Capital is now chasing platforms that can add specialized knowledge, recurring advisory relationships, and technology-enabled delivery capacity.

- Specialization Premium: CAVU, KLG, CMM, CompliancePoint, Burwood and Jefferson Wells all bring distinct practice capabilities rather than generic compliance volume.

- Wealth-Tax Convergence: Soltis’ acquisition of GDM Private Financial Solutions extends the Mercer-style precedent: PE-backed wealth platforms are using CPA tax teams to deepen household-level planning relationships.

- AI and Delivery Infrastructure: Modus and Sikich point in different directions but toward the same conclusion. The next competitive layer is not just firm count. It is the operating system: audit technology, data workflows, offshore or distributed delivery, risk infrastructure and advisory packaging.

March 2026

- MSTiller (MST) (Duluth, GA) acquired by Armanino (Further Global Capital Management). Announced March 2, 2026.

- Hucke and Associates (New York, NY) acquired by Ryan LLC (Neuberger Berman, Onex Partners, Ares Management). Announced March 4, 2026.

- CFO Hub LLC (San Diego, CA) joins CRI (Carr, Riggs & Ingram) (Centerbridge Partners/Bessemer Venture Partners). Effective March 5, 2026.

- Berman Hopkins CPAs & Associates (Orlando, FL) acquired by Doeren Mayhew (Audax Private Equity). Announced March 12, 2026.

- Price, Reuben, and Associates (Calabasas, CA) acquired by EisnerAmper (TowerBrook Capital Partners). Announced March 17, 2026.

- Accounting Specialists/ASG Advisors (Boca Raton, FL) joins Platform Accounting Group (The Cynosure Group). Announced March 17, 2026.

- SD Mayer & Associates (San Francisco, CA) acquired by Springline Advisory (Trinity Hunt Partners). Announced March 19, 2026.

- CG Advisory (Tinton Falls, NJ) acquired by Springline Advisory (Trinity Hunt Partners). Announced March 24, 2026.

- EisnerAmper continuation vehicle: Carlyle AlpInvest and Hamilton Lane join as new investors in EisnerAmper’s TowerBrook-backed platform. Announced March 25, 2026.

- Threadline Wealth (Seattle, WA), a wealth management spinoff from Moss Adams, announces strategic partnership with The Cynosure Group. Announced March 25, 2026.

As the first quarter concludes, the narrative is no longer just about who is buying whom, but about which investment philosophy—and which technology stack—will dominate the next decade.

- EisnerAmper: The Institutional Standard-Bearer.

While Citrin Cooperman led 2025, March 2026 belongs to EisnerAmper. The announcement of their Continuation Vehicle—bringing in heavyweights Carlyle AlpInvest and Hamilton Lane alongside TowerBrook—is a watershed moment. This isn’t just a refinancing; it is the creation of a “permanent capital” model that moves the firm beyond the typical five-year PE exit clock. By also tucking in Price, Reuben, and Associates this month, they are proving that their appetite for high-net-worth Southern California tax practices remains unsated. They are now the “Blue Chip” platform for partners seeking long-term stability over a quick flip.

- Springline Advisory: The Mid-Market Multiplier.

Trinity Hunt Partners’ Springline Advisory has emerged this March as the fastest-moving “New Power” in the rankings. By executing a sophisticated “coastal bookend” strategy—acquiring SD Mayer & Associates in San Francisco and CG Advisory in New Jersey within a five-day window—Springline has leapfrogged older platforms in geographic density. Their focus is surgical: they are targeting the $20M–$60M “sweet spot” firms that are too large for local players but want more personalized integration than the “Big 4-style” platforms offer. Springline is effectively building a national boutique network at scale.

- Armanino & Further Global: The Scale Specialist.

Following the acquisition of MSTiller (MST) in early March, Armanino (backed by Further Global) has solidified its position as the premier “Sunbelt” consolidator. With MST providing a massive professional engine in the Atlanta corridor, Armanino is leveraging its “Tech-First” reputation to win over Georgia-based firms wary of traditional New York-centric roll-ups. They are differentiating themselves by not just buying revenue, but by deploying a proprietary digital transformation office into every firm they acquire, instantly upgrading legacy tax practices into high-margin advisory machines.

The Strategic Shift: AI and the “Value-Added” Professional

For professionals in the CAS (Client Advisory Services) and AI space, the March data confirms a critical trend: the “Commodity Tax” era is coming to an end.

- The “Advisory Alpha”: Every deal this month—from CRI’s acquisition of CFO Hub to Doeren Mayhew’s move for Berman Hopkins—had a heavy emphasis on non-compliance revenue. The platforms are no longer valuing firms based on their audit books, but on their ability to provide “Fractional C-Suite” services.

- Platform-Wide AI Integration: We are seeing the rise of the “Universal Data Layer.” Platforms like Platform Accounting Group (which added ASG Advisors this month) are moving toward a centralized data warehouse. This allows them to run AI-driven benchmarking across their entire portfolio of thousands of small-business clients, providing insights that a standalone $10M firm could never generate.

- The Talent War: The “Head of AI” is now a standard C-suite role in these PE-backed entities. The mandate is clear: automate the 1040/1120 production cycle to free up senior talent for the high-stakes M&A and estate planning work that justifies the massive valuations being paid by Blackstone, TowerBrook, and Trinity Hunt.

February 2026

- 1RDG (Rochester, NY) acquired by Doeren Mayhew (Audax). Announced Feb. 3, 2026.

- Meritax Advisors (Frisco, TX) acquired by Ryan LLC (Ares Management; Neuberger Berman; Onex). Announced Feb. 5, 2026. Expands Ryan’s property tax valuation strategy and litigation management.

- Williams Young McKaig Ltd (WYM Rating) (Edinburgh, UK) acquired by Ryan LLC (Ares Management; Neuberger Berman; Onex). Announced Feb. 5, 2026. Expands Ryan’s UK business rates and property tax capabilities.

- Bowers Advisors (Syracuse, NY) acquired by Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Feb. 5, 2026.

- Step Up Consulting (Los Angeles, CA; $14 million est. revenue) acquired by Armanino (Further Global Capital Management). Announced Feb. 5, 2026.

- Affiniax Group (Dubai, UAE) acquired by KNAV Advisory (Nikhil Kamath). Announced Feb. 5, 2026.

- Wagner Kaplan Duys & Wood LLP (WKDW) (Englewood, CO) acquired by Richey May (F3 Partners). Announced Feb. 9, 2026.

- Liptz & Associates (Bellingham, WA) acquired by Larson Gross, a Crete Professionals Alliance platform firm (Thrive Capital/Bessemer Venture Partners). Announced Feb. 10, 2026.

- Browne Consulting Group LLC (Boston, MA) acquired by Citrin Cooperman (Blackstone). Announced Feb. 10, 2026. Deepens Citrin’s life sciences and biotech bench.

- Peltier, Gustafson & Miller (Albuquerque, NM) acquired by Capstone Accounting and Tax (Seaside Equity Partners). Announced Feb. 11, 2026.

- Thompson Palmer & Associates (Jackson, WY; two partners, eight staff) merges into McGee, Hearne & Paiz (MHP) (Ascend/Alpine Investors). Announced Feb. 12, 2026.

- Gonzalez Advisors (Irvine, CA) acquired by Elevate Platform. Announced Feb. 18, 2026.

- Richardson Kontogouris Emerson LLP (Los Angeles, CA) acquired by Cherry Bekaert (Parthenon Capital). Announced Feb. 18, 2026.

- Smeriglio Associates/Green Coast Advisors (Greenwich, CT) joins Platform Accounting Group (The Cynosure Group). Announced Feb. 19, 2026.

- CMJ LLP (Queensbury, NY) acquired by UHY (Summit Partners). Announced Feb. 20, 2026.

- Dent Moses (Birmingham, AL) acquired by Doeren Mayhew (Audax). Announced Feb. 23, 2026.

- Impact Technology Group (Birmingham, AL) acquired by Doeren Mayhew (Audax). Announced Feb. 23, 2026.

- Larson Tax Partners (St. Louis, MO) acquired by UHY (Summit Partners). Announced Feb. 25, 2026.

- Connected Accounting (CA) joins Sorren (DFW Capital). Announced Feb. 25, 2026.

February 2026 marked a decisive shift in the “Platform Wars,” characterized by massive geographic land grabs and the emergence of specialized “sub-platforms.” While 2025 was about testing the waters, February’s deal flow proves that private equity is now moving with a “winner-take-all” urgency, specifically targeting firms that bridge the gap between traditional audit and high-margin specialized advisory.

Aprio (backed by Charlesbank) executed the most aggressive maneuver of the month, effectively colonizing the Pacific Northwest by absorbing both Delap LLP and Hoffman, Stewart & Schmidt. This “double-tap” acquisition instantly transforms Aprio into a coast-to-coast powerhouse, signaling that regional dominance is no longer enough; the top-tier PE platforms are now playing for total national coverage in high-growth tech and middle-market corridors.

The mid-market also saw heavy consolidation as established platforms refined their service portfolios. Citrin Cooperman (Blackstone) deepened its life sciences and biotech bench with the acquisition of Browne Consulting Group, while Doeren Mayhew (Audax) and UHY (Summit Partners) continued their steady roll-up of regional anchors like Dent Moses and CMJ LLP. These aren’t just volume plays; they are strategic “tuck-ins” designed to layer sophisticated tax and M&A capabilities over stable, local compliance bases.

Perhaps most significant was the formal entry of the Nichols Cauley platform, backed by Madison Dearborn Partners. Led by former Baker Tilly CEO Alan Whitman, this launch introduces a “triple-threat” model—integrating CPA, Insurance, and Transaction Advisory from day one. It serves as a reminder that the “Post-Consolidation” era isn’t just about bigger firms, but about fundamentally different firm architectures designed to scale at a pace traditional partnerships simply cannot match.

January 2026

- Topping Kessler & Company (Hollywood, FL) joins PKF O’Connor Davies (Investcorp/PSP Investments). Announced Jan. 13, 2026. Expands the platform’s South Florida footprint.

- TaxOps SALT (Denver) joins Aprio effective Jan. 9, 2026. The nine-person state and local tax team is led by Judy Vorndran. (Charlesbank Capital Partners)

- Tarsus (Washington, D.C., with offices in California and Missouri; outsourced accounting and CFO advisory services) acquired by Cherry Bekaert (Parthenon Capital). Announced Jan. 13, 2026. Bolsters Cherry Bekaert’s outsourced accounting and CFO advisory practice.

- Smith Schafer (Rochester, MN) acquired by CohnReznick (Apax Partners). Effective Jan. 1, 2026. Marks CohnReznick’s entry into Minnesota.

- Scheidel, Sullivan & Lanni CPA LLC and Sierra Financial Advisors(Sacramento, CA) acquired by SAX LLP and SAX Wealth Advisors, respectively (Cobepa). Announced Jan. 7–8, 2026. SAX’s first transactions of the month.

- Sales Tax Defense (Deer Park, NY) acquired by Armanino (Further Global Capital Management). Announced Jan. 6, 2026.

- Ryan LLC (Jan. 14, 2026) reports Neuberger Berman Capital Solutions and Neuberger Berman Private Markets commit to acquire a “significant minority equity interest” for up to $1.2 billion, valuing Ryan at $7 billion. Neuberger joins Onex Partners and Ares Private Equity as minority shareholders. Closing expected in the first half of 2026.

- Rochester Tax Team (Rochester, NY) joins Modern Wealth Management (Crestview). Announced Jan. 20, 2026. Modern Wealth acquired the team from Manning & Associates.

- Riibner and Associates (Kensington, MD) joins Platform Accounting Group (The Cynosure Group). Announced Jan. 14, 2026.

- Poterack Capital Advisory (Jackson, WY; approximately $265 million in client assets) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Jan. 7, 2026.

- Owen J. Flanagan & Co. acquired by SAX LLP (Cobepa). Announced Jan. 22, 2026. SAX’s second deal of the month.

- Nichols Cauley (Dublin, GA), Partners Risk Services (Johns Creek, GA), and JGH Consulting (Atlanta) merged Jan. 5 to form a new financial services platform backed by Madison Dearborn Partners, with former Baker Tilly CEO Alan Whitman as CEO. The three-way combination launches a CPA, insurance, and transaction advisory firm from day one.

- MLCworks (New Orleans, LA) joins EisnerAmper (TowerBrook). Announced Jan. 15, 2026. Adds digital growth advisory capabilities.

- Manley Garvin (Greenwood, S.C.) acquired by UHY (Summit Partners). Effective Jan. 1, 2026. UHY’s entry into South Carolina.

- Long Run Wealth Advisors (Lake Placid, NY; approximately $640 million in client assets) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Jan. 7, 2026.

- Lancaster & Reed (Key Biscayne, FL) acquired by Doeren Mayhew (Audax). Announced Jan. 7, 2026. Establishes Doeren’s Miami international private client practice.

- Hoffman Stewart & Schmidt (Lake Oswego, Ore.) combined with Aprio effective Jan. 1, 2026, deepening the platform’s new Oregon footprint. (Charlesbank Capital Partners)

- Hess & Rohmer (Gainesville, TX) joins Sorren (DFW Capital). Announced Jan. 28, 2026. Adds to Sorren’s Texas presence.

- Herbein Financial (Reading, PA) acquired by Choreo (Parthenon Capital). Announced Jan. 21, 2026. The CPA arm — Herbein + Company — was previously acquired by Cherry Bekaert.

- Grunden Financial Advisory (Denton, TX) acquired by Allworth Financial (Lightyear Capital/Ontario Teachers’ Pension Plan). Announced Jan. 20, 2026.

- Gollob Morgan Peddy (Tyler, TX) joins Ascend (Alpine Investors). Announced Jan. 5, 2026. Adds $17 million in revenue and a strong East Texas presence.

- Gettleson Witzer & O’Connor (GWO) (Encino, CA) joins Ascend (Alpine Investors). Announced Jan. 20, 2026. Merged into the Lucas Horsfall platform firm. GWO is a family services and business management practice with a decades-long entertainment-industry client base in the San Fernando Valley.

- FSA Wealth (Needham, MA) acquired by Allworth Financial (Lightyear Capital). Closed Dec. 1, 2025; team relocated to Allworth’s Needham office. Announced Jan. 15, 2026.

- Delap (Lake Oswego, Ore.) merged into Aprio effective Jan. 1, 2026, giving Aprio its first Pacific Northwest presence. (Charlesbank Capital Partners)

- Darnell Sikes Wealth Partners (Lafayette, LA; approximately $1.9 billion in assets under management; affiliated with Darnall Sikes & Frederick CPAs) joins Avantax, a unit of Cetera Financial Group (Genstar Capital). Announced Jan. 22, 2026.

- Bradshaw Rogers (Salisbury, NC) acquired by Prime Capital (Abry Partners). Announced Jan. 22, 2026. Adds roughly $600 million AUM.

- Bowman & Company LLP (Voorhees, NJ) acquired by PKF O’Connor Davies (Investcorp/PSP Investments). Announced Jan. 5, 2026.

- Bauknight Pietras & Stormer, P.A. (Columbia, S.C.) acquired by Smith + Howard (Broad Sky Partners). Announced Jan. 13, 2026. Expands Smith + Howard into South Carolina.

- Baseline Wealth Management (London, UK) acquired by Creative Planning (TPG Capital). Announced Jan. 13, 2026. Creative Planning’s first foreign deal.

- Barb & Company and McDowell-Pearman (both Columbia, S.C.) acquired by Reid Advisors, a Crete Professionals Alliance platform firm (Thrive Capital/Bessemer Venture Partners). Announced Jan. 27, 2026. Crete’s first South Carolina presence via tuck-in.

- Alexander Almand & Bangs (AAB) (Arlington, VA) merges effective Jan. 1, 2026 with Wilson Lewis, strengthening Ascend’s Southeast footprint. (Alpine Investors)

The flurry of deals in early 2026 has officially moved the accounting industry into a “Post-Consolidation” era. The traditional “Top 100” rankings are being rewritten as private equity-backed platforms aggressively scale.

- Citrin Cooperman:The Valuation Leader. Citrin remains among the heavyweights of the PE-backed world. Following a 2025 deal with Blackstone, Citrin has moved beyond simply acquiring firms toward building a corporate enterprise model. The firm dominates the Mid-Atlantic and Northeast corridor and is using Blackstone capital to target the West Coast.

- Aprio:The Technological Aggressor. Aprio’s pro-forma revenue grew substantially in January 2026 following the HSS and Delap combinations in the Pacific Northwest. By targeting firms with strong PCAOB and cybersecurity practices, Aprio is positioning itself to compete for high-growth tech clients. Its entry into the Oregon/Washington corridor makes it a significant coast-to-coast PE platform.

- Ascend:The Identity Preserver. Ascend is among the most distinctive players. Unlike Aprio or Citrin, Ascend allows acquired firms such as Gettleson Witzer (GWO) and Alexander Almand & Bangs to maintain their local identities. Ascend is capturing the “independence-minded” segment of the market, winning deals from partners at $15M–$50M firms wary of being absorbed into a national brand.

For professionals in the CAS (Client Advisory Services) and AI space, these deals are significant because they represent a massive shift in how services are delivered. All three platforms are actively standardizing their advisory offerings around AI-enabled workflows. Aprio, for instance, is moving toward a model in which human-supervised AI handles bookkeeping, allowing advisory teams to focus on strategic tax and M&A planning.

December 2025

- Sweeney Conrad (Kirkland, WA) joins Ascend (Alpine Investors). Effective Dec. 1, 2025. Adds a presence in the Seattle metropolitan market.

- Gerald Stinnett CPA PC (Suwanee, GA) joins Doeren Mayhew (Audax). Effective Dec. 1, 2025. Doeren’s second deal in the Atlanta market, following AGL CPA Group in Duluth, GA, in July. Founder Gerald Stinnett and team transition to Doeren Mayhew’s Metro Atlanta office.

- Casey Neilon (Carson City, NV) acquired by Sorren (DFW Capital). Announced Dec. 1, 2025. Establishes Sorren’s presence in Nevada. Effective October 2025, Nicola “Niki” Neilon was appointed Chair of NASBA, leading the association’s board and guiding policy on CPA licensure, mobility, and related regulatory issues across the 55 U.S. jurisdictions.

- Berkowitz Pollack Brant (BPB) (Miami, FL) — two transactions. BPB’s wealth management practice joined Baker Tilly (Hellman & Friedman) effective Dec. 1, 2025. A second BPB transaction closed Dec. 15, 2025, further expanding Baker Tilly’s South Florida footprint.

- Wolf Maryles & Associates (New York, NY) acquired by PKF O’Connor Davies (Investcorp/PSP Investments). Announced Dec. 2, 2025. Team joined the New York office effective Jan. 1, 2026.

- Burt Wealth Advisors (North Bethesda, MD) acquired by Creative Planning (TPG Capital). Announced Dec. 2, 2025. Adds approximately $1 billion AUM and establishes a North Bethesda hub.

- Glass Jacobson Wealth Advisors (Baltimore, MD) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Dec. 2, 2025. Adds approximately $1 billion AUM and deepens Mid-Atlantic presence.

- DK Partners (Austin, TX) acquired by Carr, Riggs & Ingram (Centerbridge Partners/Bessemer Venture Partners). Joined Dec. 3, 2025. CRI’s fifth merger since receiving PE funding in late 2024.

- The Vroman Group (West Des Moines, IA) acquired by BGM (Unity Partners). Announced Dec. 3, 2025.

- Marshall Financial Group (Doylestown, PA) acquired by Creative Planning (TPG Capital). Announced Dec. 9, 2025. Adds $900 million-plus AUM to the platform.

- Farkouh Furman & Faccio (New York, NY) acquired by Prosperity Partners (Unity Partners). Completed Dec. 9, 2025. Serves as Prosperity’s flagship New York City office.

- Mark Rule & Co. (Butte, MT) acquired by Capstone Accounting & Tax (Seaside Equity Partners). Joined Dec. 10, 2025. Expands Capstone into the Montana market.

- Brown and Bakondi (Oregon City, OR) and Watters and Associates(Roseburg, OR) both join Platform Accounting Group (The Cynosure Group). Announced Dec. 11, 2025. Two Oregon additions in a single day.

- RTO & Company (The Dalles, OR) joins Sorren (DFW Capital). Announced Dec. 15, 2025.

- Seghetti Waxler/Bayshore Advisors (Santa Cruz, CA) and Wayne Long & Co./Longview Advisors (Bakersfield, CA) both join Platform Accounting Group (The Cynosure Group). Announced Dec. 24, 2025. PAG closed four deals in December alone.

- North Star (Snohomish, WA) acquired by Capstone Accounting & Tax (Seaside Equity Partners). Joined Dec. 29, 2025. Strengthens Capstone’s Washington state presence.

- Geographic Land Grab: Florida and the Mid-Atlantic (Maryland/DC) were the primary battlegrounds in December, with major players like Baker Tilly, Creative Planning, and Mercer Advisors aggressively acquiring local market leaders.

- Wealth + Accounting Synergy: Firms like Mercer and Creative Planning are increasingly targeting accounting-heavy RIAs (like Glass Jacobson Wealth) to offer “connected” tax and wealth services.

- Employee Ownership Models: Unity Partners (via Prosperity) is utilizing a “Purpose Plan” for employee ownership to differentiate its acquisition model from more traditional PE structures.

November 2025

- Mize CPAs Inc. (Topeka, KS) — including Prism Financial, which manages $1.8 billion AUM — acquired by Aprio (Charlesbank). Effective Nov. 1, 2025. Adds 20 partners and 300-plus professionals.

- BiggsKofford (Colorado Springs, CO) joins Ascend (Alpine Investors). Announced early November 2025.

- Pesta Finnie & Associates (Charlotte, NC) acquired by Frazier & Deeter (General Atlantic). Announced Nov. 4, 2025. Strengthens real estate tax and family office expertise in Charlotte.

- Smart Accountants and Infinity Globus (both Ahmedabad, India) acquired by Springline Advisory (Trinity Hunt Partners). Completed Nov. 5, 2025. Offshore delivery centers acquired directly rather than outsourced — a shift toward owning global delivery capability.

- Rosen Sapperstein & Friedlander (RS&F) (Towson, MD) joins Frazier & Deeter (General Atlantic). Announced Nov. 5, 2025. Deepens Frazier & Deeter’s Mid-Atlantic footprint.

- Gatto Pope & Walwick (San Diego, CA) acquired by Citrin Cooperman (Blackstone). Announced Nov. 6, 2025. Adds 10 partners and more than 60 professionals.

- Mennenga Tax & Financial (Madison, WI) acquired by Merit Financial Advisors (Constellation Wealth Capital). Effective Oct. 31, 2025; widely reported in early November.

- Novotny CPA Group (Grand Rapids, MI) acquired by Doeren Mayhew (Audax). Effective Nov. 10, 2025. Partners Randy Novotny and Tom Winkelman joined as principals.

- KBFM (Nashville, TN) acquired by Citrin Cooperman (New Mountain Capital). Announced Nov. 11, 2025.

- Beach Freeman Lim & Cleland (El Segundo, CA) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners). Announced Nov. 12, 2025. Adds 20 tax professionals and offices in El Segundo, Irvine, and Ontario, CA.

- Accuity LLP (Honolulu, HI) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Nov. 13, 2025. Crete’s first Hawaii presence.

- TBK CPA (Houston, TX) joins Doeren Mayhew (Audax). Effective Nov. 17, 2025.

- McMurray Fox (Nashville, TN) acquired by Doeren Mayhew (Audax). Effective Nov. 17, 2025.

- BGM (Bloomington, MN) acquired by Prosperity Partners (Unity Partners). Announced Nov. 17, 2025.

- Richardson & Co (Medway, MA) joins Ascend via Walter Shuffain (Alpine Investors). Effective Nov. 20, 2025. Integrated into the Boston-area Walter Shuffain hub.

- John G. Burk (Keene, NH) joins Ascend via TSS Advisors (Alpine Investors). Effective Nov. 21, 2025. Expands TSS Advisors’ footprint across Northern New England.

Global Talent Plays: The Springline acquisition of Smart Accountants and Infinity Globus highlights a shift toward acquiring offshore delivery centers in Ahmedabad, India directly rather than outsourcing to them.

Wealth-Accounting Convergence: Acquisitions such as Prism Financial (by Aprio) and Beach Freeman Lim & Cleland (by Mercer) demonstrate that the line between high-net-worth tax work and asset management continues to blur.

October 2025

- Shorepoint Capital Partners (Norwood, MA; $850 million AUM) acquired by Allworth Financial (Lightyear Capital/Ontario Teachers’ Pension Plan). Effective Oct. 1, 2025.

- Singer Burke (Los Angeles, CA; $1.2 billion AUM) acquired by Mercer Advisors (Genstar Capital/Oak Hill Capital/Altas Partners) and integrated into Mercer’s ultra-high-net-worth Regis Group. Announced Oct. 7, 2025.

- Herbein + Company (Reading, PA) acquired by Cherry Bekaert (Parthenon Capital). Announced Oct. 8, 2025. Note: Herbein’s affiliated wealth management practice — Herbein Financial — was separately acquired by Choreo in January 2026.

- AVL Growth Partners (Boulder, CO) acquired by Ampleo (Unity Partners). Announced Oct. 15, 2025.

- TKR Advisors (Arlington, VA) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Oct. 22, 2025.

- Nissen & Meyer (Redmond, OR) acquired by Capstone Accounting and Tax (Seaside Equity Partners). Announced Oct. 23, 2025. Expands Capstone’s Central Oregon presence.

- Healthworks (Los Angeles, CA) joins Sorren (DFW Capital). Announced Oct. 29

- Parthenon Capital – Backing Cherry Bekaert. Since investing in Cherry Bekaert in June 2022, Parthenon has fueled over 15 acquisitions, including the Herbein + Co. deal.

- Seaside Equity Partners – Backing Capstone Accounting and Tax. Based in San Diego, Seaside focuses on “mission-critical” services in the Western U.S. They partnered with Capstone in April 2025 using a $325 million investment vehicle and directly supported Capstone’s acquisition of Nissen & Meyer in October 2025.

- Oak Hill Capital – Backing Mercer Advisors alongside Genstar Capital and Altas Partners. Oak Hill has been an ownership partner in Mercer Advisors since 2019. This backing has enabled Mercer to scale to over $69 billion in assets, facilitating large acquisitions like Singer Burke.

- Lightyear Capital – Backing Allworth Financial. Lightyear is a specialist in financial services PE and provides the capital for Allworth Financial’s aggressive “hub-and-spoke” acquisition model, which includes the Shorepoint Capital deal.

September 2025

- Richey May (Denver, CO), WSRP (UT), Moss Krusick & Associates(Winter Park, FL), USX Advisors (Seattle, WA), and Sobul, Primes & Schenkel (CA) combined Sept. 9, 2025 to form a national platform backed by F3 Partners. Pre-deal, Richey May ranked No. 102 on the IPA Top 200 with $57.7 million in revenue. The combined entity vaulted into the Top 50.

- Auxis (Coral Gables, FL) acquired by Grant Thornton Advisors (New Mountain Capital). Closed Sept. 2, 2025.

- KSDT (Miami, FL) acquired by Ascend (Alpine Investors). Announced Sept. 3, 2025. Ascend’s largest merger to date at the time — adds five offices, 29 partners, and 276 professionals.

- Horton Lee Burnett (Birmingham, AL) acquired by Smith + Howard (Broad Sky Partners). Announced Sept. 3, 2025.

- ORBA (Ostrow Reisin Berk & Abrams) (Chicago, IL) acquired by Citrin Cooperman (Blackstone). Announced Sept. 4, 2025.

- Mauldin Vaught (Fayetteville, AR) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Sept. 8, 2025.

- Prism Financial (Overland Park, KS; $1.8 billion AUM) acquired by Aprio (Charlesbank). Announced Sept. 19, 2025. Note: Prism is also referenced in the Mize CPAs entry for November — verify whether these are two separate transactions or a single deal reported in stages.

- Carson & McKinney (Nashville, TN) acquired by Doeren Mayhew (Audax). Announced Sept. 22, 2025.

- Advisent (San Diego, CA) joins Crete Professionals Alliance (Thrive Capital/Bessemer Venture Partners). Announced Sept. 18, 2025.

- Dhruva Advisors (Mumbai, India) — Ryan LLC (Ares Management) takes a majority interest/JV stake. Announced Sept. 29, 2025. Ryan’s India market entry.

- Schulman Lobel (New York, NY) joins SAINVUS. Announced Sept. 30, 2025. SAINVUS is a founder-led family office platform, not a traditional PE-backed roll-up.