But They’ll Take the Money.

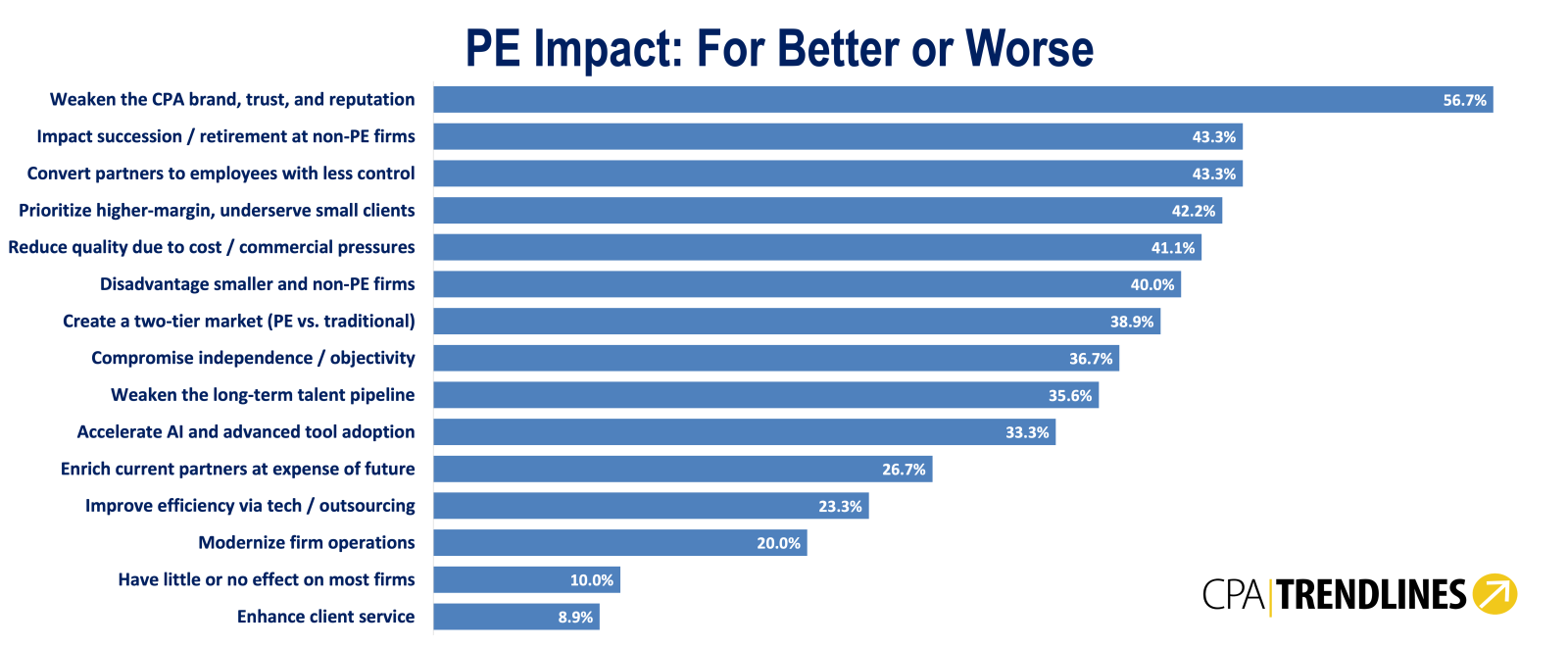

Most CPAs are concerned that private equity is undermining the CPA profession’s reputation for independence and objectivity. Only 10% say PE will have little or no impact. Fewer still can say PE will improve client service. (CPA Trendlines)

By CPA Trendlines

As the CPA Trendlines CPA PE Deal Tracker™ adds 13 more closings for the month of May, a new survey shows accountants worrying about PE tarnishing the image and reputation of the profession. But half say they might take the money anyway.

MORE Private Equity | MORE All 500-plus Headline Deals for the Last 10 Years

The CPA PE Deal Tracker™ now contains more than 500 headline deals and developments. Through May 31, the tracker shows 91 headline 2026 events, including 83 M&A deals. Full-year 2025 finished with 190 significant events, including 178 M&A deals. The last three consecutive months have produced the first sustained plateau in 12-month trailing M&A activity since the acceleration phase that began in 2023.

Meanwhile, nearly half of the professionals in the new CPA Trendlines survey — 49.5 percent — describe themselves as decidedly opposed to private equity investment: fiercely independent, not interested, never ever.

The rest, a bare but discernible majority, are not. They would do a deal for the right price. Or they are already in play. Or have already done a deal.

“It only makes sense to keep our options open,” says Michael Royer of Royer Advisors and Accountants in Falmouth, Maine. He is not opposed, and he is not sold, adding “it’s still a personal business — and we don’t know the full impact of AI.”