Firms gear up for advisory, grapple with retirements, and take aim at bigger competitors.

By CPA Trendlines Research

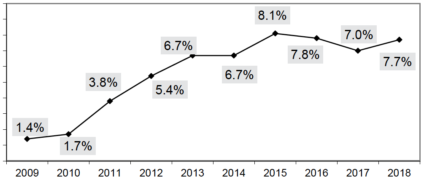

The Rosenberg MAP Survey

In the new 2019-2020 edition of the annual Rosenberg MAP Survey, the leading national benchmarking study for firms of all sizes, the average firm is growing at 7.7 percent, up from 7 percent in last year’s study and reversing a two-year decline.

Meanwhile, organic growth, excluding mergers and acquisitions advanced to 5.9 percent from 4.3 percent, “proving that the accounting profession is really cultivating a focus on business development efforts,” according to the authors, led by Charles Hylan of The Growth Partnership and Marc Rosenberg of Rosenberg Associates, who founded the study 21 years ago, making it the longest-running such benchmarking project in the profession. (And available from CPA Trendlines here.)