On revenue gains of 11.8%

By Charles Hylan

Rosenberg MAP Survey

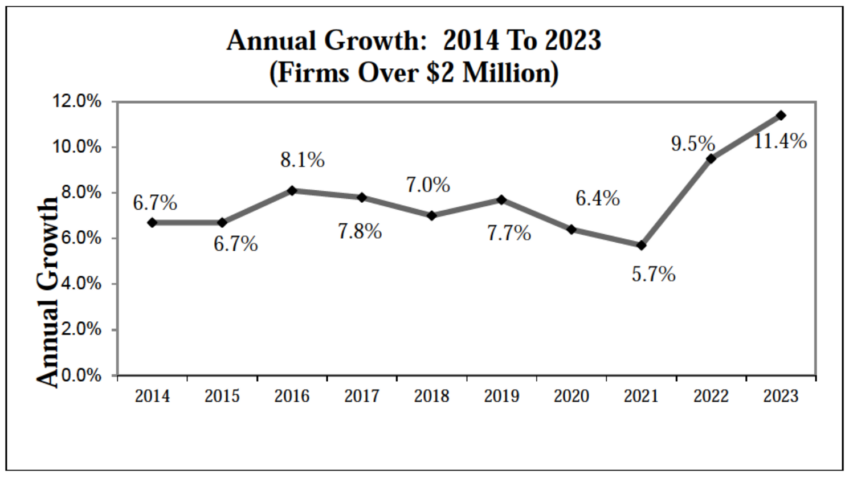

It’s been another amazing year for the accounting profession! But – it comes at a price. As we look at the firms in our survey with revenue greater than $2 million, income per partner was up 11.8%, and revenue was up 11.4%.

MORE in SURVEYS & RESEARCH: Firms Rev Up Expansion Plans | Overcoming the Five Hurdles to Advisory Services | Research: Accounting Pros Cautiously Optimistic about Generative AI | Why Compliance Still Matters. But It’s Not Enough. | New Businesses Mean New Business | How to Transform Your Team into Trusted Advisors

Exclusively for PRO Members. Log in here or upgrade to PRO today.

This is the second year in which profits grew faster than revenue.

This new revenue and additional profits are occurring amidst a severe staffing shortage, resulting in people being stretched to their limits.

So, how do we keep this going at less of a “price tag?”

Doing nothing is not an option, and hope is not a strategy.

Our profession is experiencing unprecedented pressure from the economy, staffing shortages, technology, and competition.