Busy Season 2026 sets up a year of tough decisions about monumental transformations.

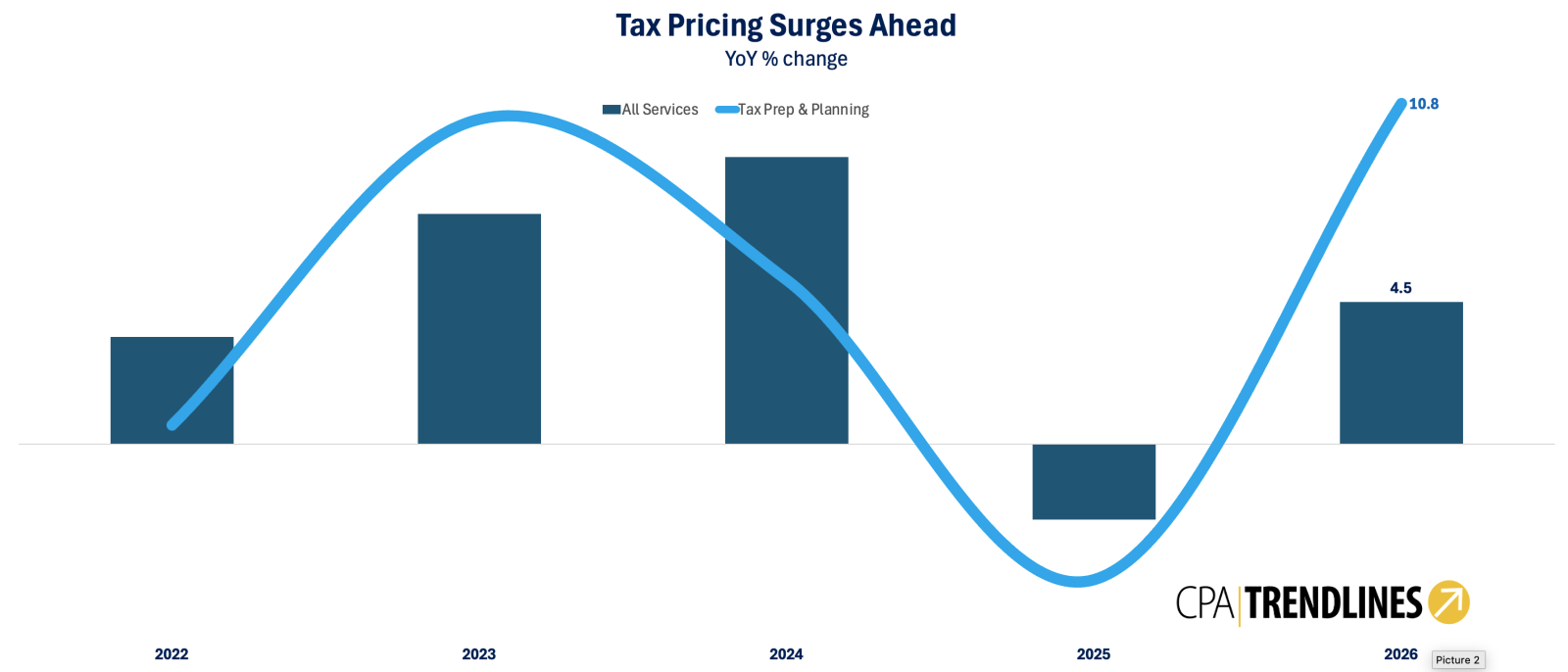

Busy Season 2026: Billing rates for tax prep and planning are increasing at a 10.8% year-over-year rate, rushing past the average tax and accounting fee increase of 4.5%.

By CPA Trendlines

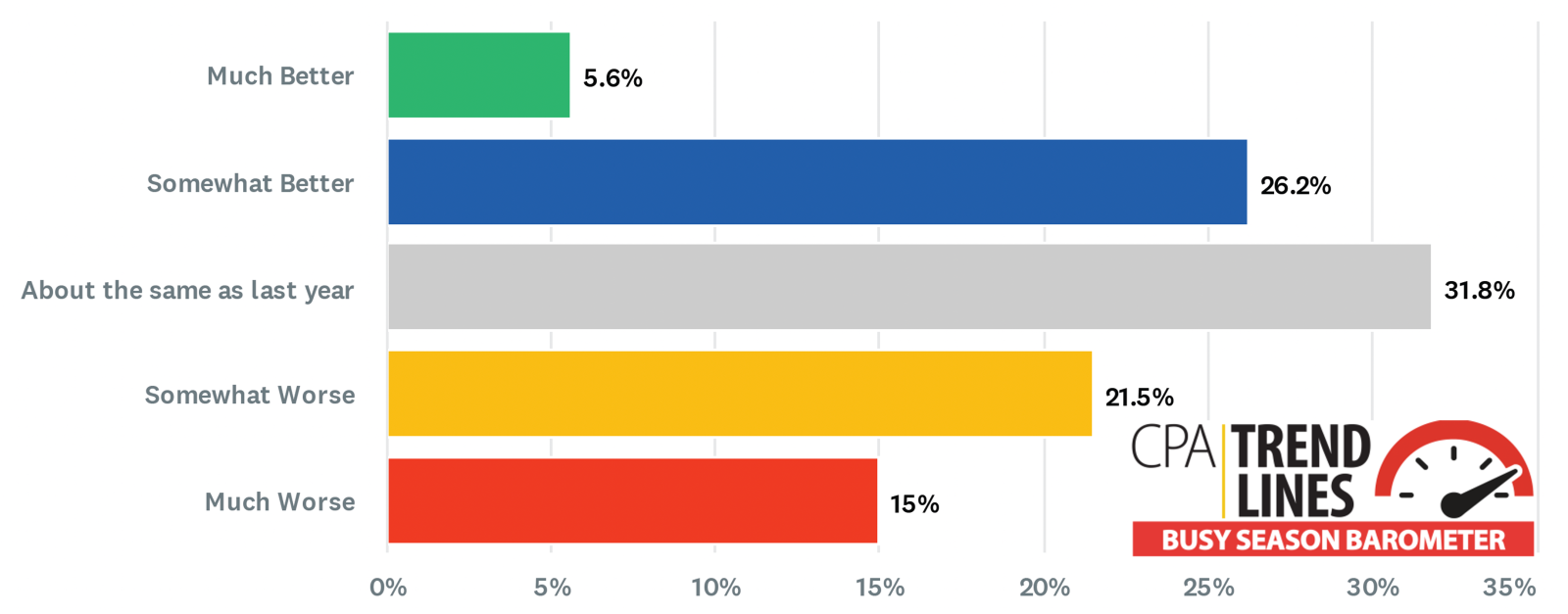

Busy Season 2026: Tax professionals struggle to improve systems and metrics, with “much worse” beating “much better” by three to one.

As tax season 2026 comes to a close, new data show that price hikes for tax prep and planning are running at double-digit rates, even as billing rates for most other accounting services are flattening out, according to new CPA Trendlines research in conjunction with the annual Busy Season Barometer.

Tax practitioners are finishing the season as a divided profession, with fewer than 6% reporting a “much better” year, against almost three times that many reporting a “much worse” year.

Coming out of tax season, many firms are facing major decisions in the coming months driven by new artificial intelligence investments, a fundamental shift in staffing models, and private equity disruptions.