Advisory and specialty services lead the way.

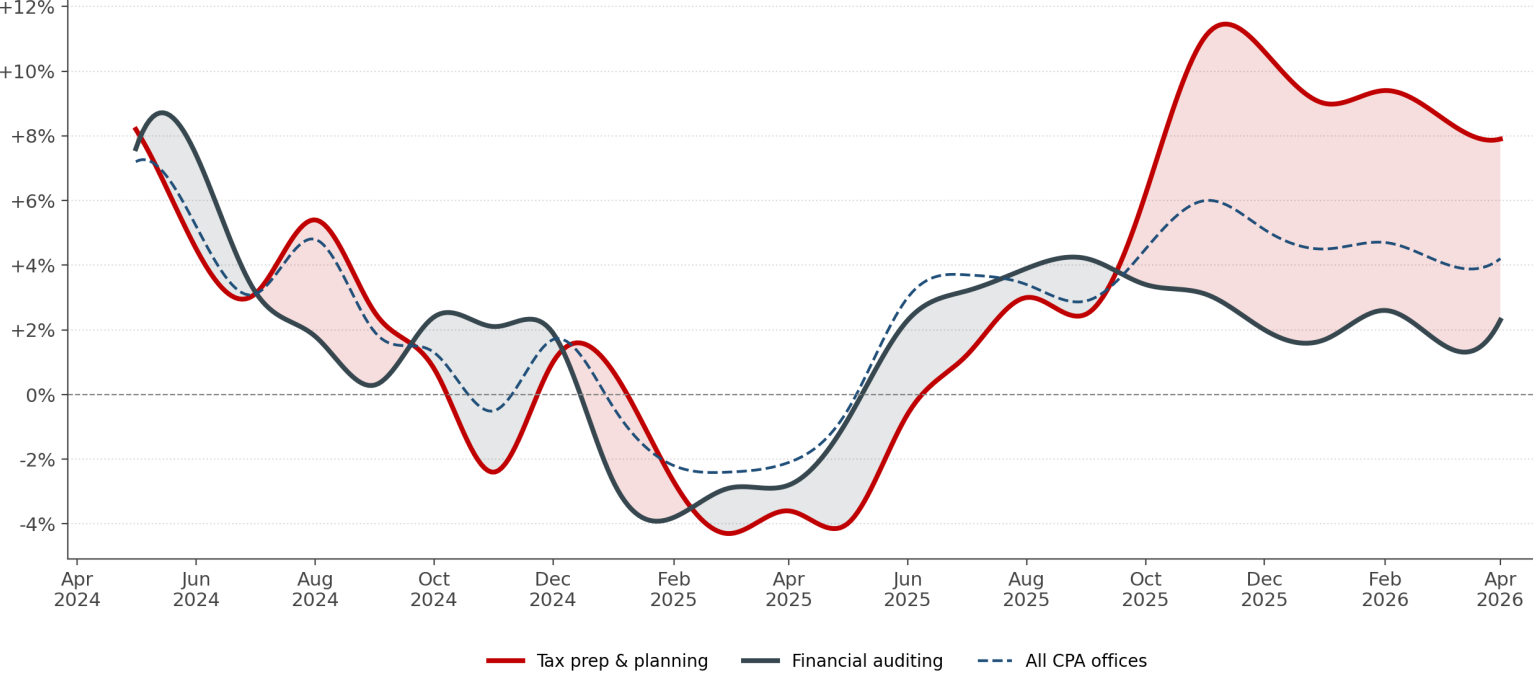

Tax pricing pulls away from audit, year-over-year percent change. (CPA Trendlines)

By CPA Trendlines

After two years of mostly weak pricing power, accounting firms appear to be regaining the initiative on billing rates, led by tax services with eye-popping 8% increases.

MORE in Pricing: Tax Prep Billing Rates Lift Busy Season | The Hidden Data Behind CPA Firm Burnout and Profit Pressure | Six Steps to High-Value Tax Advisory |

CPAs are raising rates by 4.2 percent year over year, reversing a 2.1 percent decline recorded a year ago, according to new CPA Trendlines findings.

Tax prep and planning lead the sector, with a 7.9 percent increase. Advisory-oriented work is climbing at a 6.3 percent rate. Core CPA firm services are gaining at a 4.9 percent pace. Financial auditing is advancing just 2.3 percent.

The divergence between tax audit first shows up in the data in October 2025 when CPA firms started sending 2026 tax-season engagement letters with new rates, and it was the first cycle in which firms had both a fresh tax code to interpret.

Meanwhile, audit pricing has been suppressed by procurement scrutiny, audit-committee fee oversight, and standards-led commoditization.

Busy season 2026

The new trend lines reinforce a point many firm leaders have been making privately for months: clients are resisting routine fee increases for standardized compliance work, but appear more willing to pay for tax planning, advisory guidance and specialized expertise.

Industry pricing surveys point in the same direction.

Ignition’s U.S. Accounting and Tax Pricing Benchmark reports that 80 percent of firms expect to raise prices again in 2026, with many shifting toward value pricing and fixed-fee engagement structures. Hourly billing is retreating, dropping to under 4 percent of firms in 2025 from nearly 8 percent in 2024, according to the same report.

CPA Trendlines reports that tax prep billing rates are “rushing past the average tax and accounting fee increase,” with busy-season pricing running materially ahead of broader accounting inflation.

Billing for complexity

The underlying drivers are becoming easier to see.

Labor shortages are pressuring firms even as accounting employment stabilizes. While CPA firms are shrinking their headcount, the broader accounting sector is hiring,

Capstone Partners investment bankers describes the accounting services market as caught between widespread labor shortages and rising demand for CPA, tax and advisory services, conditions that have driven heavy merger-and-acquisition activity across the sector.

Tax complexity appears to be building in the wake of the One Big Beautiful Bill Act, signed into law in July 2025. The legislation makes many of the expiring Tax Cuts and Jobs Act provisions permanent while layering in a new set of provisions scheduled to sunset in 2028.

The result is a tax code that practitioners must now re-map for nearly every closely held business and individual client. Implementation guidance, planning opportunities and rate-table reconciliations remain works in progress more than ten months into the new regime.

The tech edge

Today’s environment tends to favor firms with deep tax expertise and advisory capabilities.

It also helps explain the growing divergence between tax pricing and audit pricing.

Tax increasingly functions as a strategic planning business. Audit, by contrast, remains more exposed to competitive bidding pressure, procurement scrutiny and standardized workflow processes. Firms may still command premium pricing in specialized assurance niches, but routine audit work remains comparatively price-sensitive.

Bookkeeping and compilation pricing occupies a middle ground, charting 3.1 percent increases, slower than tax and advisory work but still positive.

Technology may also be reshaping the pricing landscape.

Routine transactional work is becoming increasingly automated through cloud accounting platforms, workflow systems and artificial-intelligence-assisted coding tools. Higher-value planning, judgment and interpretation work appears to be retaining strong pricing leverage.

Pricing power

Today’s looser pricing conditions come as a welcome relief for the many firms that spent 2024 struggling to preserve margins. Inflation cooled. Technology costs climbed. Clients challenged annual increases. At the same time, firms were paying up for experienced managers, tax specialists and advisory talent.

Today, many firms are responding by tightening billing rate discipline, pruning low-margin client relationships and shifting toward higher-value advisory work. The latest pricing data suggest at least some of those efforts are beginning to show up in national industry statistics.

Even so, the recovery remains measured rather than explosive. It suggests clients are still pushing back against broad-based fee inflation.

For firms attempting to balance staffing shortages, technology investment and profitability, the new pricing environment offers a modest but important sign of stabilization.

For clients, it likely means tax and advisory bills will be rising faster than traditional audit and compliance work.

And for the profession as a whole, it’s clear that pricing power now follows specialization.