Accounting Firms Face a Productivity Test as Demand Outruns Capacity.

Accountants Demand Index: Steady Growth in New Work

By CPA Trendlines Research

The tax and accounting profession’s biggest problem is no longer finding work. It is finding the time, people, and technology to do it.

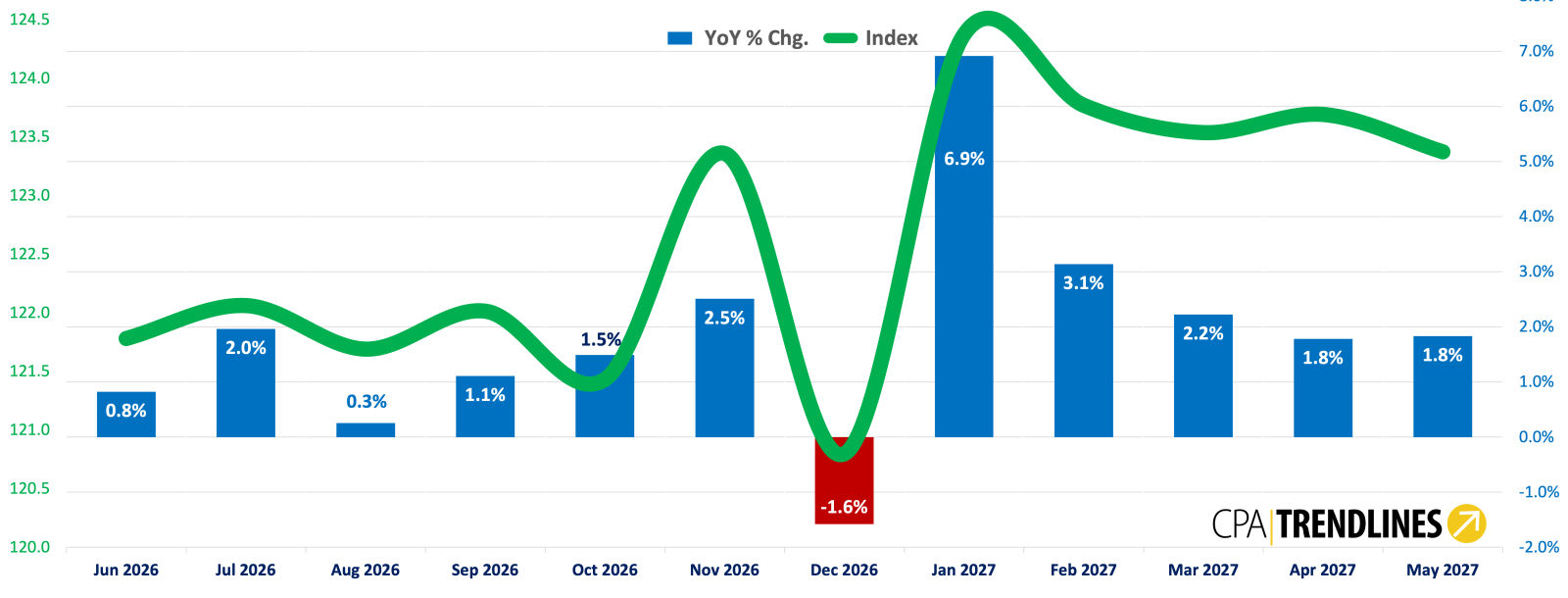

The new CPA Trendlines Accountants Demand Index, which slipped in May, remains firmly above year-ago levels. The proprietary index of economic indicators fell to 121.2 in May, down 0.3 percent from April but still up 1.8 percent from a year earlier and comfortably above its 2019 baseline level of 100.

The next six months are forecast to follow a pattern firm owners will recognize. June softens. July surges with the sharpest single-month gain in the forecast window. Then August stalls, nearly flat, which is where the index makes its call.

History says late summer is the reset. This year, the data says the reset holds: the index climbs steadily through September, October and into November, reaching its fall peak before December pulls it back below zero.