Webinar, May 13: Due Diligence for Private Equity

Independence vs. Transacting: The Facts Behind Each Pathway,

with Bob and Doug Lewis, Visionary Group

May 13, 4-5 pm ET

Register here | Learn more

Independence vs. Transacting: The Facts Behind Each Pathway,

with Bob and Doug Lewis, Visionary Group

May 13, 4-5 pm ET

Register here | Learn more

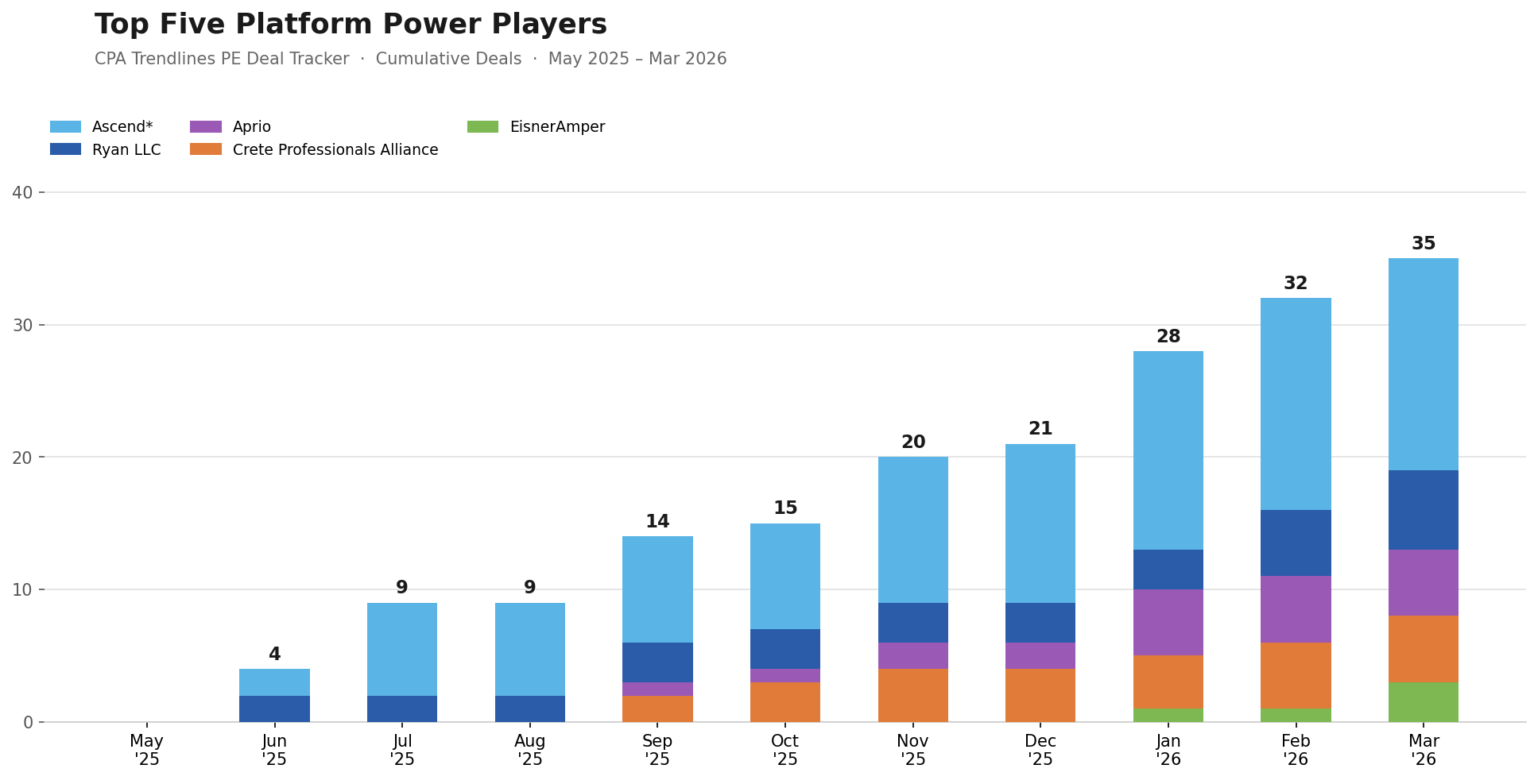

After hundreds of deals, the data show a gravitational pull toward a handful of buyers now driving the profession’s future.

By CPA Trendlines Research

The frantic pace of deal-making in March has officially transitioned the accounting industry from a “consolidation phase” into a “platform war.”

As the first quarter concludes, the narrative is no longer just about who is buying whom, but about which investment philosophy—and which technology stack—will dominate the next decade.

The conventional narrative about private equity in accounting says capital is flooding in, the profession is democratizing, and every CPA firm in America can access institutional money for the first time. But the cold, hard data tells a different story.

MORE in Private Equity | Alan Whitman Plants a Flag in the Private Equity Landscape | The PE Takeover: Audit Problem? What Audit Problem? | The 7.6x Machine: How Grassroots Firms Are Taking Private Equity for a Ride | Why the Next Big CPA Firms Won’t Look Like CPA Firms

Of the 427 transactions logged in the CPA Trendlines PE-CPA Deal Tracker™ since 2016, more than 200 — nearly half — are concentrated in just 10 platforms. That challenges the notion of a market open to all.

The idea that PE would spread evenly across hundreds of firms, like a broad revolution, is, in the actual deal flow, a rapid gravitational implosion around a handful of mega-aggregators that are vacuuming up firms faster than the rest of the market combined. The acceleration curve alone should unsettle anyone clinging to the idea that this market is still nascent. READ MORE →

There are a lot of decisions to make.

By Marc Rosenberg

CPA Firm Mergers: Your Complete Guide

Most firms find that it takes three to four years to fully implement a merger. But during the first few months after the effective date of the merger, there are quite a few administrative and procedural things that need to be attended to immediately.

Most firms try to get as much of a head start as possible, before the effective date of the merger.

READ MORE →

Don’t concentrate on some and breeze through others.

By R. Peter Fontaine

NewGate Law

My approach in writing this post is to give you a comprehensive list of due diligence items for your consideration, and to let you select the reviews you wish to perform. The ultimate decision rests with you.

The scope of due diligence will differ depending on the transaction, and should be appropriately tailored. However, your Letter of Intent combined with the six areas outlined below result in a fairly comprehensive list of due diligence procedures that should serve the needs of most CPA mergers.

READ MORE →

It’s a favor, so negotiate generously.

By Marc Rosenberg

CPA Firm Mergers: Your Complete Guide

A Practice Continuation Agreement (PCA) is a written contract between a sole practitioner and another firm for the latter to take over the solo’s practice, either permanently or temporarily, in the event of a sudden, unexpected event that prevents the solo from working, most commonly a health issue.

Logically, it would make total sense for every one of the 30,000 sole practitioners in the U.S. to have a PCA in place. After all, the solo has no other partners to take her place and in the vast majority of cases, the solo’s staff doesn’t have the skill level or the certifications needed to run the practice in the absence of the owner.

READ MORE →