The Most Comprehensive Practice Manual Ever Written on Partner Performance, Pay, and Incentives

By Marc Rosenberg, CPA

This monograph compiles all of Rosenberg’s compensation know-how and resources. Based on more than 20 years of experience in devising partner comp systems with hundreds of firms – large and small, from coast to coast, with partners earning $200,000 to $1 million.

Price range: $305.00 through $350.00

The Most Comprehensive Practice Manual Ever Written on Partner Performance, Pay, and Incentives

By Marc Rosenberg, CPA This monograph compiles all of Rosenberg's compensation know-how and resources. Based on more than 20 years of experience in devising partner comp systems with hundreds of firms – large and small, from coast to coast, with partners earning $200,000 to $1 million.TO READ THE FULL ARTICLE

Continue reading your article with a CPA Trendlines Pro membership.

Links to download your PDF will appear on the order confirmation screen after purchase and in your email receipt from auto-confirm@cpatrendlines.com.

* Rosenberg PDFs are read-only – no printing, markup, reproduction, or further distribution. Downloadable to five personal devices.

The most authoritative, comprehensive handbook on the subject

Partner compensation is the Holy Grail of CPA firm practice management. Firms have eternally searched for an income allocation system that is the fairest of all, makes everyone happy, is easy to administer and rewards performance.

From Marc Rosenberg’s proprietary consulting handouts to interviews with managing partners from some of the nation’s best-managed firms, and including dozens of articles and blogs published on this topic, this monograph presents everything your firm needs to evaluate and design your partner comp system.

Beginning, intermediate and advanced guidance include:

• Partner Comp 101

• How To Design a Partner Comp System

• The 12 Systems Used By All Firms

• Open vs. Closed Systems

• Comp Committee vs. Formula Systems

• The Role of the Book of Business

• Differences Between Large And Small Firm Systems

• The Managing Partner’s Compensation

• Trends And Controversies

• Best Practices

Tough Issues, Smart Answers

- What Partners REALLY Earn and How They Earn It

- Partner Compensation 101

- Designing A Partner Comp System

- Performance-Based Subjective Systems

- Partner Compensation Formulas

- Non-Performance Based Systems

- Other Partner Comp Systems

- Open vs. Closed Comp Systems

- The Declining Importance of the Book of Business.

- Crash Course: Operating A Compensation Committee

- Integrating Partner Comp with Strategic Planning

- How Large and Small Firms Allocate Income

- The Managing Partner’s Comp

- Partner Evaluations

- Data Used to Evaluate Partner Performance

- Compensation Nuances: The Devil Is in The Details

- Does Compensation Motivate Performance?

- Trends and Controversies in Partner Compensation

- Case Studies

- Pearls of Wisdom

Plus: Three Appendices

- Appendix A: Partner Compensation Best Practices

- Appendix B: Partner Compensation System Features

- Appendix C: Partner Compensation Questionnaire

It’s an Art, Not a Science

When partners use the term “partner compensation,” they may be referring to either or both of the following:

- The system used to determine each partner’s income for the year.

- Partners’ earnings— the share of the firm’s total income allocated to them.

Unless stated otherwise, partner compensation or partner income includes all forms of remuneration such as base salary, draw, bonus, final distribution, interest on capital and other related terms. It does NOT include fringe benefits and perks. But it includes deductions from partners’ pay, such as voluntary contributions made to qualified retirement plans and contributions made to a firmwide funded partner buyout plan.

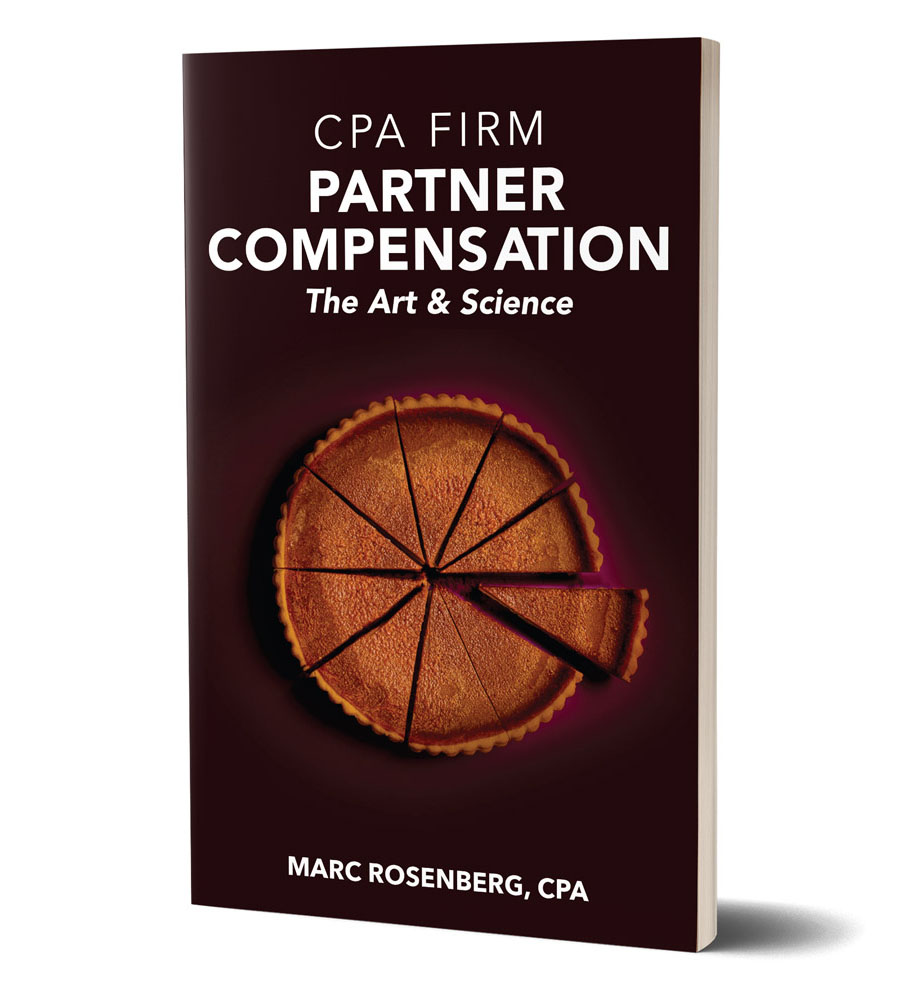

Pies: a great metaphor for partner compensation

A firm can have the most unfair, biased, and illogical system known to man, but if the pie (total income to the partners), also known as the profits of the firm) is sizable, the partners will be easier to please because their slice of the pie will most likely be pretty satisfying.

On the other hand, a firm can have the fairest, most accurate, logical system ever invented, but if they’re dividing up a small pie, many partners will be unhappy with their tiny slice.

The lesson: If partners are unhappy with the compensation system and firm profitability is low, they should focus more on increasing firm profitability than perpetually looking for a better way to allocate income. They will never be satisfied with a small slice of pie.

But this lesson is not easily learned. Most CPA firm partners come from humble backgrounds. Their families may not have been in the poor house, but it’s unlikely they were wealthy. When partners think about the annual income they earn ($300,000 to $500,000 or more for many of them), a smile comes across their faces because, in their wildest dreams, they never thought they would earn this kind of money. But that grin turns instantly into a grimace when they find out that another, less deserving partner earned more.

Get the picture? Partner compensation is much more than a mere number that shows up on a K-1:

- It’s a de facto summation of a partner’s worth to the firm.

- It’s a form of rating or ranking the partners.

- It’s a reward for hard work, performing well and achieving goals.

- It’s the money needed to enable partners to support their families and maintain a certain style of living.

For these reasons, partner compensation is easily the most sensitive and hotly debated aspect of CPA firm practice management. This topic appears often on conference agendas. It’s frequently written about in publications. Its what partners talk about in the hallways and in the privacy of their offices.

The allocation of partner income is much more an art than a science. Anyone who thinks otherwise is either naïve or has never been a partner whose income was subjected to an income allocation process.

Partner compensation is not science. If allocating partner income were a science, it would be easy to concoct the perfect formula that factors in all relevant performance metrics, both tangible (production) and intangible (leadership, mentoring staff, loyalty, teamwork, etc.), producing results that would be considered fair and acceptable to most or all partners. There would be few arguments among the partners because they would feel the formula says it all and leaves nothing for debate.

But alas, there is no such thing as a perfect partner compensation formula. No system has been invented that (a) is 100% fair in the eyes of all the partners, and (b) is a proper blend of tangible and intangible performance factors. Some firms sarcastically say that the acid test of a good system is one that makes every partner a little unhappy. I don’t subscribe to this because it is quite possible to create a system that will satisfy all partners. The goal of this monograph is to show you how this is done.

Partner compensation is an art because it needs to factor in a host of tangible and intangible performance attributes, such as:

- Basic production metrics.

- Evaluation of partners in official management and leadership roles such as MP, PICs, Board and Compensation Committee members and practice leaders.

- Major intangible factors such as developing staff, teamwork, loyalty and work ethic. There is no empirical guide to weighing these factors.

- Nuances and subtleties of partner performance.

- The extent to which partners delivered what the firm needed and expected from them.

- Determining the proper breakdown of amounts to comprise income tiers such as interest on capital, base, and bonus.

- The balance between a partner’s historical performances and performance for the current year.

- How certain partners view their own compensation compared to that of others.

Balancing the allocation of income between objective, traditional production metrics with subjective performance factors, though certainly not rocket science, is not easy and is fraught with complexity. It’s an art.

– Marc Rosenberg, CPA

About Marc Rosenberg, CPA

CPA Trendlines commentator Marc Rosenberg is a nationally known consultant, author, and speaker on CPA firm management, strategy, and partner issues.

President of his own Chicago-based consulting firm, The Rosenberg Associates, he is the founder of the most authoritative annual survey of mid-sized CPA firm performance statistics in the country, The Rosenberg Survey, also available from CPA Trendlines.

He has consulted with more than 700 firms throughout a consulting career spanning more than 20 years. Accounting Today magazine annually acknowledges Marc Rosenberg as one of the 100 most influential people in the CPA profession, and INSIDE Public Accounting has repeatedly recognized him as one of the ten most recommended CPA firm consultants in the country.

See more: Marc Rosenberg at CPA Trendlines

CPA Firm Partner Compensation: The Art and Science

Price range: $305.00 through $350.00

You may also like…

-

TOUGH QUESTIONS, SMART ANSWERS

TOUGH QUESTIONS, SMART ANSWERS 202 Questions and Answers: Managing an Accounting Practice, The Complete 2-Volume Set

Complete Two-Volume Set

By Edward Mendlowitz, CPA, ABV, PFS

With tables, checklists, sample letters, illustrative examples, real-life stories, step-by-step instructions, and appendix.

Price range: $199.95 through $299.95 Learn More -

HERDING CATS

HERDING CATS How to Engage Partners in the Firm’s Future

The secrets every leader needs to know

$99.95 Learn More -

RUN with the BIG DOGS

RUN with the BIG DOGS 8 Steps to Great

By Domenick J. Esposito, CPA

The practice management handbook for achieving unbeatable branding, rapid growth, and extraordinary profits.

Price range: $279.95 through $299.95 Learn More